***** denotes well-worth reading in full at source (even if excerpted extensively here)

Economic and Market Fare:

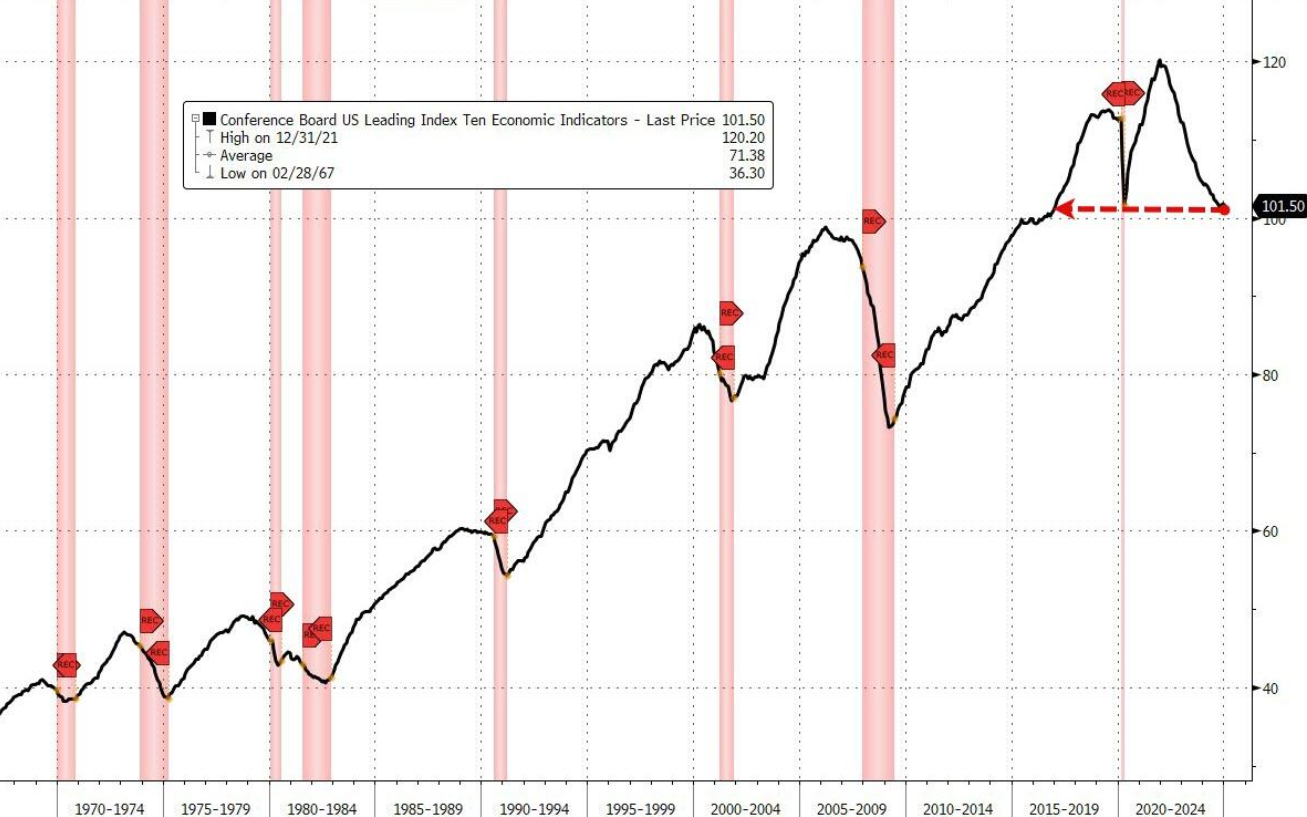

The incoming economic data remains strong. But we are starting to worry about the downside risks to the economy and markets from: 1) the impact of DOGE layoffs and contract cuts on jobless claims and 2) persistently elevated policy uncertainty weighing on capex spending decisions and hiring decisions. .............

Bassman: Got Duration?

............................................. This opinion does not contradict the prior 7 pages, rather I will say the Bond Bull is simply a more efficient manner to access Duration.

Bubble Fare:

............................................. This opinion does not contradict the prior 7 pages, rather I will say the Bond Bull is simply a more efficient manner to access Duration.

The Bond Bull is the “151 proof” of duration assets; a 15%-dollar allocation will match the duration of the Aggregate Bond Index.

Instead of the standard 60%/40% portfolio, consider 70% stock, 10% Credit, 10% Commodities, and 10% the Bond Bull.

For Hedgers, one should use the Bond Bull not because you know rates will decline, but rather because you are bearish, and might be wrong.

Remember: For most investments, sizing is more important than entry level.

Bubble Fare:

Forget the damage to markets when the passive bid dries up and the Fed is stuck cutting rates into stagflation. The psychological damage will be worse.

............... It’s difficult to ignore that Tom Lee has “nailed it” on markets over the last decade, and I need to give credit where it’s due. Holding your nose and buying stocks without giving a single solitary fuck about valuations or the macroeconomy has sadly been the most effective way to generate returns over the last decade or two. But as every piece of financial literature you’ve ever read says somewhere on it: past performance is not indicative of future results.

And people that don’t make daily appearances on CNBC — like, oh, say, Warren Buffett, for instance — are taking another road: getting into cash.

Maybe it’s a just a coincidence?

Though the tune of buying the dip has hardly changed, the environment it’s being sung in has. Stocks now trade at a Shiller PE that’s approaching 40x, a level only eclipsed once in history during the 2000s dot-com bubble.

But if the market’s price-to-earnings ratio and the macroeconomy didn’t matter when stocks were trading at 30x earnings, why should they matter with stocks trading at 40x earnings?

This indifference to valuations—helped along by the “passive bid” of 401(k)s and ETFs consistently buying the market at any given price (well explained by Bill Fleckenstein here on Julia LaRoche’s podcast, and then updated here during his appearance last week), combined with what is widely perceived to be an unlimited Fed put, combined with the unprecedented amount of liquidity doled out as a result of COVID, combined with the stock market becoming accessible to literally any human being on earth that wants to take their shot thanks to the advent of retail trading apps—has distorted expectations and psychology not just about the stock market, but also about the basic fundamentals of economics and finance, in a way that many of us probably would not have even thought fathomable 50 years ago.

Modern monetary theory has acted like a risk-hunger marijuana edible that all traders and investors have been forced to swallow, resulting in an insatiable, decades long case of the market munchies.

In fact, liquidity has been so ubiquitous and markets have been so rigged that people are speculating upwards of $3 trillion in an asset class — crypto — that, to the best of my understanding, offers very little product or service and exists almost entirely digitally.

If you want to try to make the argument that overvalued equities can sometimes be hard to recognize, especially when they only seem to continue to go up and valuations only seem to continue to expand, that’s one thing. But how, with a straight face, can anyone argue that $3 trillion worth of crypto is in some way “undervalued,” let alone serves a purpose at all? ............

********** Hussman: The Government Deficits Land in the Deepest Pockets

Should you change your investment position here? We haven’t. Whether or not we’re at a market peak, we were already defensive based on extreme valuations, unfavorable internals, and overextended conditions. If you’re a passive investor, my intent is not to encourage you to abandon your discipline. What I do believe, however, is that this is an extraordinarily good moment to examine your risk exposures and to take them seriously. If your notion of passive investing doesn’t allow for a realistic possibility of a market loss well in excess of 50%, or a decade or more in which the S&P 500 lags Treasury bills, you’ve not only decided to be a passive investor, you’ve decided to ignore history. So, whatever your discipline, examine your risk exposures.It’s helpful to keep in mind that anytime you change part of your investment position, there will be regret. If you sell part of your holdings, and the market continues to advance, you’ll regret having sold anything. If you sell part of your holdings and the market declines, you’ll regret not having sold more. The same is true for purchases. There will always be regret. The key is to realize this up front, and choose an acceptable level of regret. You do that by examining your exposure to risk, considering both potential returns and potential losses.

With our most reliable valuation measures more extreme than both the 1929 and 2000 market peaks, we continue to believe that the stock market is tracing out the extended peak of the third great speculative bubble in U.S. history. Since the initial January 2022 market peak, the equal-weighted S&P 500 has clocked a cumulative total return less than 2.4% ahead of Treasury bills, while the small-cap Russell 2000 has lagged T-bills by more than -10.6% since then. The capitalization-weighted S&P 500 Index has performed better during this period only by driving the price/revenue multiple of the information technology sector to levels that easily exceed the 2000 extreme.

While record valuations, unfavorable market internals, and recurring warning flags have held us to a bearish outlook since the June comment, You Can Ring My Bell, our investment discipline has benefited despite a further market advance since then, partly as a result of the hedging implementation we introduced in the fourth quarter (see the section titled “Good News and Good News” in the October comment, Subsets and Sensibility).

What appears to be an endless bull market advance is actually a classic two-tiered blowoff in speculative glamour stocks. If you missed Bill Hester’s excellent analysis of large-cap market concentration, Slimming Down a Top-Heavy Market, now may be a worthwhile opportunity to recognize how extreme the current situation has become. The chart below offers some sense of how much investors now need to rely on a “permanently high plateau” in valuations. ............

While valuations are extremely informative about likely 10-12 year market returns, as well as the potential depth of market losses over the completion of a given market cycle, valuations are not reliable indications of shorter-term market outcomes. Investor psychology – particularly speculative psychology versus risk-aversion – has an overwhelming impact on shorter-term market outcomes. Since speculators tend to be fairly indiscriminate, and increasing selectivity has historically preceded the most severe market losses, our most reliable gauge of speculation versus risk-aversion is the uniformity of market internals ..............

........... On the economic front, it’s worth reviewing our current position in the economic cycle. Investors may not entirely appreciate is that U.S. real GDP is now running 2.7% above its sustainable full employment potential as estimated by the Congressional Budget Office (CBO). The CBO estimate is closely aligned with our own estimates that simply use productivity and labor force demographics, so while one might find a little bit of wiggle room in the estimates, real potential GDP has generally been a reliable guide to the general position of the U.S. economy within the economic cycle.

...

Recessions are first and foremost periods when a mismatch emerges between what the economy has been producing, and what the economy now demands. Those mismatches can be driven by shifts in consumer preferences, interest-sensitive investment, technology, government spending, credit strains, or crises like the pandemic. Disruptions triggered by these mismatches take time to resolve, absent massive bailouts and deficit spending. It’s not just the direct disruptions, but the broader uncertainty that they produce, that contribute to economic downturns.

In my view, we’re suddenly soaking in exactly this sort of disruption. Keep your eye on financial markets, credit spreads, and surveys of purchasing managers and consumer confidence. Emphatically, further deterioration would be needed in order to expect a recession with confidence, but the thresholds are surprisingly close. Indeed, just 5% lower in the S&P 500, 15 basis points wider in Baa credit spreads, and 1 point down in the ISM Purchasing Managers Index would be sufficient to move our Recession Warning Composite into the red. More sensitive composites have been hovering at their own thresholds for some time, but they’re prone to occasional false signals. As usual, our preference is to draw a common signal from multiple measures, without relying on any single component. ................

.............................................

From 2016 through 2020, $8.4 trillion in new 10-year deficit spending was approved – a combination of tax cuts and net spending increases, with about $3.6 trillion of that related to pandemic response. From 2020 through 2024, another $4.3 trillion in 10-year deficit spending was approved, about $2.1 trillion of that being pandemic response (Committee for a Responsible Federal Budget). Government deficits, again, are always matched by surpluses in other sectors. In recent years, the primary beneficiaries have been business profits and household savings, though the household savings have gradually been spent down, largely becoming business profits as well.

With regard to the record ratio of financial market capitalization to GDP, the government deficits of the past eight years have bloated the corporate profits on which investors are placing extreme price/earnings multiples while calling it “stock market capitalization.” Meanwhile, the highest income earners have also accumulated the cash and securities that the government issued to finance the deficits. As a result, the massive deficits of recent years are a significant portion of what the deepest pockets presently call “wealth.” .................................

Vid Fare:

Michael Hudson, Alexander Mercouris & Glenn Diesen

Charts:

1:

BofA: Is the S&P 500 expensive? $SPY

— Mike Zaccardi, CFA, CMT 🍖 (@MikeZaccardi) February 20, 2025

Statistically speaking, 19 of 20 metrics give an emphatic affirmative response pic.twitter.com/xIvVAOaoCp

(not just) for the ESG crowd:

That’s the assumption underlying the decision to keep capitalism in place even as we watch our biosphere disappear before our eyes, and it’s pure fantasy. As long as mass-scale human behavior is driven by the pursuit of profit, you’re going to see the interests of humanity and the ecosystem subverted by that pursuit. .................

U.S. B.S.:

........ And the thing about this genre of tweet is that they’re kind of right — Obama didn’t have any “scandals” of the level we see from Trump. But the fact that the evil things Obama did weren’t considered scandalous says profoundly ugly things about the kind of society we are living in.

Obama committed all kinds of atrocities while president that would be considered scandalous if we lived in a world that is even remotely sane. Destroying Libya and leaving it a smoldering crater of humanitarian disaster. Tearing apart Syria with the dirty war that featured pouring weapons into the arms of al-Qaeda affiliates. Initiating the US-backed incineration of Yemen. Lighting the fuse for the ruination of Ukraine with the US-backed regime change op in 2014. His notorious drone program. The list goes on. .................

Lawrence: “Trump crosses the Atlantic.”

Eight years ago, at precisely this moment in Donald’s Trump’s first term, the new president was pushing his case for a restored détente with Russia. Trump went on to summit with Vladimir Putin five times and conducted at least 16 telephone exchanges with the Russian president.

This was the count by mid–2019. After that and until the end of his term, the Deep State—notably the intelligence apparatus, the Democratic National Committee, and the mass media—had Trump bound in the rope of subterfuge so thoroughly that the relationship developed no further.

The neo-détente Trump favored—that Trump was correct to favor, better put—never came to be. Joe Biden and his people, to state the obvious, were by contrast neo–Cold Warriors—mere ideologues, neoliberals wholly incapable of autonomous thought, initiative, imagination, or anything else that sophisticated statecraft requires of its practitioners.

................. In this context, extricating the U.S. from the Ukraine quagmire is more than a footnote but nothing like the main attraction. Assuming all goes to Trump’s apparent plan—and we must make this assumption with unsparing caution—the center-stage attraction is discarding what has passed for a world order since the 1945 victories ................

...................... The panic easily detected among the Continent’s besieged elites, whose leaders have convened twice this week for emergency summits in Paris, has also been legible, pitifully enough, in the press coverage of Munich and Trump’s various demarches. All I have read in corporate and state-sponsored media on both sides of the Atlantic has been shockingly distorted, featuring more than the usual measure of outright lies.

Vance spoke in favor of neo–Nazi and “far-right” parties. (He went nowhere near the topic.) The Trump–Putin telephone call was all about the Russian leader’s cynical manipulations and Trump’s appeasement. (It was about the restoration of workable bilateral relations.) Trump has opened the door for “Putin” to advance through Europe. (He entertains no such ambition.) “Putin’s” objective is to destroy the European Union and NATO. (Ditto.) ..................

The End may be further away than you think.

............... As I write, the ground in Europe is still vibrating from the shock, and the political and media classes are still trapped between incredulous disbelief and barely-concealed anger that any such thing could have happened. They are still trapped in Cliché Land (“abandoning Ukraine”) and it may be some time before anything resembling reality actually penetrates their skulls. But in the meantime, and while we wait for some kind of rationality to gain a limited purchase, there are a couple of general points to make, and then I will get more deeply into the question of “talks.”

The first is the belief that the apparent disengagement of the US from Ukraine will actually make much difference. The only way in which this would be true is if a Ukrainian victory (generously defined) would be possible with further US assistance, but not without it. ................................

.......... The anger now arises from the fact that the pretence and discourse of eventual western victory have been officially undermined by the US, and so cannot be sustained any longer. ................................

Yascha Mounk and Wolfgang Münchau discuss the failure of the German model.

***** Israel And Its Apologists Weaponize Sympathy In Order To Facilitate Genocide

Sci Fare:

Evolution itself can evolve, new study argues

A new computer model suggests that the process of evolution can get better at evolving in the face of environmental change

Activist and author Yves Engler has been jailed by Montreal police for criticizing media figure Dahlia Kurtz and her support for Israeli atrocities in Gaza, after Kurtz said Engler’s comments made her feel “afraid for my safety”.

After Engler wrote about the charges against him, he reported that he was subsequently charged for “harassing the police” by drawing public attention to his case.

It’s fascinating how everyone who supports Israel always collapses into playing the victim at the earliest opportunity—even western police forces tasked with persecuting Israel’s critics. Israel models this victim-LARPing behavior, and its entire goon squad follows its example. ............

........................ The real currency of our world is not money or resources, nor gold, nor even weapons. The real currency of our world is narrative and the ability to control it, because if you can control the narrative, you can control everyone.

The average human life is dominated by mental stories, so if you can control the stories that humans are telling each other about their world, you can control the humans. ....................

Sci Fare:

A new computer model suggests that the process of evolution can get better at evolving in the face of environmental change

Other Fare:

No comments:

Post a Comment