*** denotes well-worth reading in full at source (even if excerpted extensively here)

Economic and Market Fare:

While the world’s eyes were on the pandemic, China and the war in Ukraine, the paths to prosperity and shared interests have grown murkier.

When the world’s business and political leaders gathered in 2018 at the annual economic forum in Davos, the mood was jubilant. Growth in every major country was on an upswing. The global economy, declared Christine Lagarde, then the managing director of the International Monetary Fund, “is in a very sweet spot.”

Five years later, the outlook has decidedly soured.

“Nearly all the economic forces that powered progress and prosperity over the last three decades are fading,” the World Bank warned in a recent analysis. “The result could be a lost decade in the making — not just for some countries or regions as has occurred in the past — but for the whole world.” ....

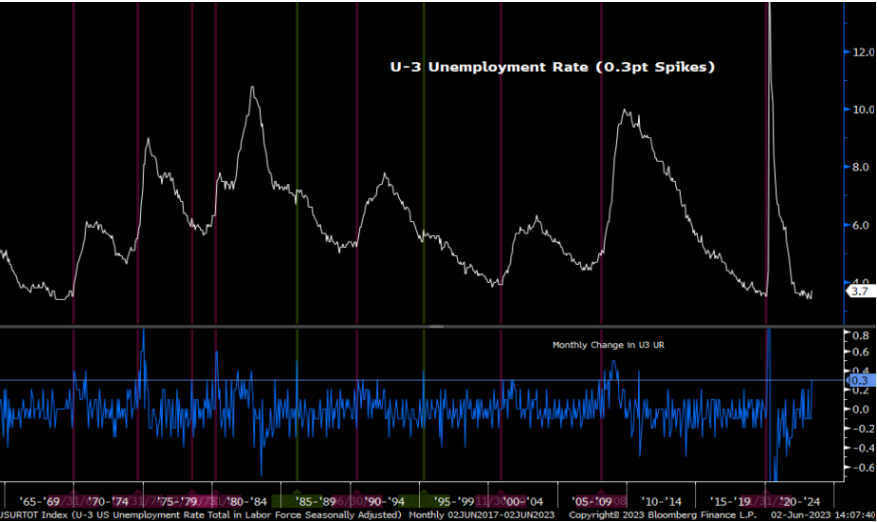

Guggenheim: A Fed-Induced Recession Is Still in the Pipeline

CLOs’ appetite for debt wanes due to limits on purchases, pushing up cost of capital as economy slows

...... Over the past decade the market for leveraged loans has become a critical funding source both for US companies and private equity groups snapping up businesses. The shift has been particularly significant because banks have curtailed some of the lending they did before the financial crisis. ......

Citi says S&P 500 net positioning 'most extended ever'

in which, apparently "ever" means "going back to 2010"

in which, apparently "ever" means "going back to 2010"

......... Many macro factors affect asset prices; principally, they are growth, inflation, and liquidity. Based on current and forward-looking measures, we think growth is not a supportive factor to equities and has not been for a while. Our cyclical rotation strategy, which seeks to avoid recession risk in equities, remains in cash.

There is a range of reasons one might be long equities at this junction— disinflationary market pricing, liquidity improvements, short-term regime dynamics, or perhaps even bubble-timing alpha. However, cyclical growth is not one of them. Indeed, our ETF portfolio has been long equities for a while now, as it considers various factors in executing positions. However, we think it is essential that investors understand the risk they underwrite when they buy equities at this junction— it’s not because real growth dynamics are likely to accelerate from here.

A quarter of workers surveyed by PwC expect to change jobs in the next 12 months, up from 19% last year, as they are increasingly left cash-strapped in a cooling economy while dealing with inflationary pressures.

Even as the 'Great Resignation' continues, around 42% of the employees surveyed by PwC in its new study of the global workforce said they are planning to demand payrises to cope with the higher cost of living, up from 35% last year.

Some 46% of respondents to the '2023 Hopes and Fears Global Workforce Survey', which polled 54,000 workers in 46 countries, said either that their households were struggling to pay bills every month, or that they could not pay bills most of the time. ...Milanovic: The Great Convergence

Global Equality and Its Discontents

Money Fare:

One of the things which alternately frustrates me and fascinates me is the mythology surrounding the idea that the central bank can address inflation by manipulating the price of money, even if it ignores the quantity of money.

I say “mythology” because there is virtually no empirical support for this notion, and the theoretical support for it depends on a model of flows in the economy that seem contrary to how the economy actually works. The idea, coarsely, is that by making money more dear the central bank will make it harder for businesses to borrow and invest, and for consumers to borrow and spend; therefore growth will slow. This seems to be a reasonable description of how the world works. But this then gets tied into inflation by appealing to the idea that lower aggregate demand should lower price pressures, leading to lower inflation. The models are very clear on this point: lower growth causes less inflation and more growth causes more inflation. The fact that this doesn’t appear to be the case in practice seems not to have lessened the fervor of policymakers for this framework. This is the frustrating part – especially since there is a viable alternative framework which seems to actually describe how the world works in practice, and that is monetarism. .......

*** Keen: Money From Nothing

.................................. Libertarians might instinctively prefer private money creation (Credit) over government (Fiat), because the former involves free choice and the latter involves compulsion. But from a practical point of view, the “free choice” generates compulsion while the “compulsion” option generates freedom.

Quotes of the Week:

Credit money creation effectively forces the non-bank private sector into negative equity. Banks, by definition, have to have non-negative equity: if their assets exceed their liabilities, they are bankrupt. Bank lending generates positive equity for the banks, and it therefore necessarily generates negative equity for the non-bank private sector: if banks have financial assets that exceed their liabilities, then by the logic of double-entry bookkeeping, non-banks have identical negative financial equity.

This reality of private money creation is, I believe, a major reason why banks can entice us into speculation on the value of non-financial assets—things like houses and shares—which we buy with yet more borrowed money. We end up with asset bubbles and speculation dominating true enterprise.

On the other hand, though no-one enjoys paying taxes, if a government routinely spends more than it takes back in taxation, then the non-government sector gains positive financial equity—which is precisely equal in magnitude to the negative financial equity of the government sector. This effectively creates “free money” for the non-bank private sector, which allows it to undertake commerce on its own terms, without necessarily having to borrow from banks in the first instance.

Figure 7 shows a “pulse” of Credit money creation, followed by a pulse of Fiat money creation. Though you’ll need to run the model yourself to see this clearly (I’ll post it on Patreon and link to it on Substack), when the credit money pulse stops, so does expansion of the economy. However when the fiat money pulse stops, growth continues because the interest paid on government bonds continues to create money.

If we could just get our heads around these practical realities of money creation, and throw the myths of Neoclassical and Austrian economists into the rubbish bin of history where they belong, then the monetary side of capitalism would function a damn sight better than it has under the last forty years of Neoliberalism.

Quotes of the Week:

Privorotsky: "I wonder if we will look back on that as a prescient signal of a very durable economy or a local high of exuberance relative the range of uncertainty for the back half of the year."

Charts:

1:

Charts:

1:

In his 2004 letter to shareholders, Warren Buffett provided Lou Simpson’s track record with GEICO’s portfolio under the title of “Portrait of a Disciplined Investor”:

(not just) for the ESG crowd:

Robust reporting principles to improve today’s carbon-trading markets

Summary.

Markets for carbon trading function poorly, and many traded offsets do not actually perform as promised. Without robust protocols for monitoring offsets and in the absence of proper accounting mechanisms, market-based approaches to reducing atmospheric GHG will be vulnerable to misrepresentation and fraud.

This article presents an accounting framework based on five core principles. The first two define what can and cannot be counted as an offset and what may or may not be traded. The remaining principles set out basic accounting guidelines for offsets. Together they provide the foundation for a well-functioning market that accelerates innovation and deployment of improved offsetting technologies, leading to atmospheric decarbonization.

Average sea surface temperature surrounding Europe's seas reached all-time high

We’d need to use a huge amount of ocean space to get even close to hitting targets

Ethics:

Lab-grown meat as a way out of our greatest ethical dilemma

................................ Our species has an ethical obligation to move beyond factory farming. It would be a shame if our unwillingness to honestly confront what we do to animals causes us to compound our crimes by delaying the day that we do.

Other Fare:

The rise of the BRICS group is directly linked to the decline of the US dollar says a top economist.

Economist Richard Wolff told Sputnik that the US displaced its mother country Britain as the world's dominant imperial power around 1920 — and that history was now repeating itself.

"The American empire didn't work the same way. It didn't set up colonies the way the British had in India or South Africa or any of the other places," Wolff said. "It had a more informal empire. [From] The way it had managed to control Latin America throughout the early years of this country to how they expanded and controlled the world by economic arrangements, by political deals, by alliances."

But the US empire peaked around the year 2000, the academic said, and is now in "decline."

"We lost the wars in Vietnam. We lost the war in Afghanistan. We lost the war in Iraq," Wolff said. "It's not clear what's going to happen in Ukraine. But I wouldn't bet money on a different outcome there either. And that war is a war between the United States and Russia more than anything else, with the disaster being concentrated on [...] Ukraine."

While the US leads the G7 group of the biggest Western economies, "there's a different and other bloc, and that's what's new, it's the bloc called the BRICS." ...

A delegation of African leaders traveled to Russia and Ukraine to urge for a ceasefire and negotiations

QOTW:

Snyder: Why is the mainstream media so quiet about the fact that Joe Biden and his family received tens of millions of dollars from foreign nationals in an influence-peddling scheme that went on for many years while Biden was vice-president