US unemployment is high (near 10%) and core inflation is low (near 1%) so Fed needs to remain very accomodative; in fact, a Taylor Rule prescription suggests FOMC s/b at -5% or so right now, so, relative to where they should be, the Fed is as TIGHT as it ever has been in the AG/BB era

---> Fed on hold through 2012, likely longer, as per Japan

BoC caught between rock and hard place: doesn't want frothy domestic housing and household debt markets to turn into dangerous bubbles, so would like to be more restrictive, but knows external demand will highly influence economy, and risks there growing significantly

---> BoC will hike in July and likely again in September, getting to 1%, by which time the U.S. and global economic outlooks will have deteriorated sufficiently to keep BoC on hold indefinitely

U.S. economic outlook is gloomy for a number of reasons (with or without the European problem); paraphrasing

from Andy Harless:

1. quantitative easing, which was temporarily buttressing demand, is over (for now) imparting a downward bias to growth in the coming quarters (before QE gets revived again)

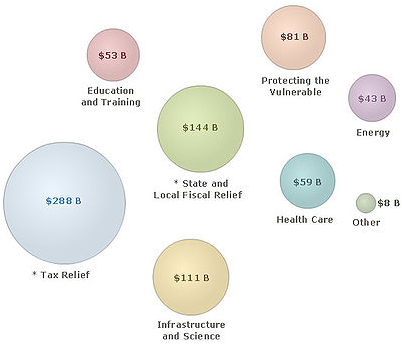

2. fiscal stimulus has been largely exhausted (

see recent post) so that its impact will be declining in the coming quarters, imparting a downward bias to growth; even if additional stimulus funds are come up with, they are likely to be modest given the political climate and the paranoia about fiscal deficits (legitimate concern for Mediterranean countries in Euro, but for US, like Japan before it, not yet a legitimate concern), such that any future stimulus will be less than past stimulus, so will have declining impact on GDP growth regardless

3. pent-up demand from consumers (many of whom were worried about the losing their jobs last year but no longer are) has been largely exhausted, and its impact will likely decline over time, imparting a downward bias to growth in the coming quarters.

4. inventory adjustment process has run its course (manufacturing inventories are actually quite elevated relative to shipments/sales); significant increases in production are no longer necessary to maintain inventories, so while inventories added significantly to Q4/09 and Q1/10 growth, may detract, and certainly not add, to H2 growth.

5. recent dollar strength and weak external demand (particularly Europe, but anticipate slowing elsewhere as well, including BRICs) mean export growth will not drive robust recovery.

6. normally, the surge in productivity at the beginning of a recovery is followed by a surge in employment, with a lag of about two quarters; there has been no employment increase following last year’s surge in productivity (exempting census jobs, which, added in spring, will be lost by autumn); meanwhile, productivity growth has settled back into the normal range, which dampens hope for a future surge in employment.

7. Bush tax cuts expire at the end of 2010, which will be drag on income growth and thus on economic growth starting six months out

8. a housing double dip is soon arriving, as government stimulus for housing market, which temporarily supported house sales data, has been lost, and banks will need to increase the pace of foreclosure activity, and there is substantial shadow inventory already; and prices, though they have fallen substantially, remain above their long-term norms in terms of price-to-income and price-to-rent ratios, and can be expected to revert below their means given supply overhang, high unemployment, flat income growth, etc. (

see T2 Partners' presentation)

9. the next wave of the credit crisis is ramping up right now; the first wave was subprime, whereas this wave is option ARM

10. consumer balance sheets remain extremely stretched; the process of deleveraging has just begun, and will take many many years to be complete

11. state and local government budgets are severely impaired; these governments, some of which are already in crisis mode, will act like 50 little Hoovers going forward; state and local government spending is 50% larger than federal government spending; has acted as drag on growth in recent quarters, at an escalating pace, and given that fiscal year ends are June 30 and new budgets need to be pared back, the pace of contraction will escalate further

x. there is no evidence of any positive stimulus to growth that would offset all these negatives; in fact, the Consumer Metrics and ECRI leading indicators are already flagging potential of double-dip, and those indicators have been steadily deteriorating over recent weeks/months, with no signs of turning around; even the Conference Board's LEI, once you extract stock prices, yield curve and money supply growth, were negative in 2 of last 3 months

xi.

as per Hussman, when you have had credit spreads widening over 6 months, in conjuction with stock prices down over 6 months, in conjunction with a moderate or flat yield curve, in conjunction with an ISM of 54 or below and moderate or declining employment growth, a current or imminent recession has been flagged without error in every instance (i.e. each those criteria is not particularly notable by itself, but in conjunction they are very notable); all the conditions are met with the exception of the ISM

---> U.S. double-dip

Canada is the tail that gets wagged by the U.S. dog; as goes their economy, so goes ours, although with more volatility; for more on Canada,

see past post.

as per the

Edward Chancellor piece (or

brief summary here), I believe China is a bubble waiting to pop, a la Japan 1989 or US 1999; its growth has not just been supported by government stimulus, which, arguably, could continue indefinitely, but also by extraordinary and unhealthy credit growth, by a housing bubble, and by over-investing in yet more excess capacity (malinvestment), none of which are sustainable; its just a matter of (indeterminate) time before they pop and cause major headaches

I have long anticipated, and

continue to anticipate the Japan scenario, or one much like it, to play out in the U.S.: i.e. once the BoJ was under 1%, it stayed there; and 10-year bond yields have been at or under 2% for over a decade; there has been deflation for 15 years; the Nikkei is at a quarter the level of its peak, and half the level it was at 10 years ago; money multiplier and velocity contraction have more than offset any money supply growth; real estate prices have been trending down persistently since the peak; consumption has been flat for over a decade; nominal GDP is at the same level it was at 18 years ago

even in the absence of a double-dip in the U.S. (which i DO expect), unemployment resolutely above its normal rate (NAIRU) is disinflationary, and we already have core CPI at 1%, which, i believe, posits strongly for deflation; even if one took the Fed's central tendency forecasts of unemployment and inflation for 2010/11/12, as per the SF Fed, the

Fed should be on hold into 2012 (taking account of QE) or through 2012 (assuming no QE)

none of this is good for stocks; all is good for bonds (and gold!)

stocks remain overvalued; forward P/E ratios are worse than useless; on a forward P/E basis, stocks are fairly valued, at just under 15 ---- but fwd P/E has been between 14 and 15 non-stop for the last 5 years!!!

forward earnings estimates are pricing in huge advances in E, not at all consistent with a modest GDP growth environment, much less a double-dip or Japan scenario

longer-term measures of valuation more clearly show how overvalued the stock market is; the Q-ratio, relative to its long term average, shows the S&P about 35% overvalues; the cyclically-adjusted P/E ratio (using 10-year average earnings) shows similarly (CAPE is north of 20, relative to long-term average of 16ish)

based on E of 60 and P/E of 15, fair value of S&P is 900ish

given that I predict another downleg for the economy, I anticipate that analysts will again overreact on the downside (as they did when S&P hit 666), and S&P will trade in 800s again in next 9 months

S&P/TSX will trade in kind

GoC 10years will trade south of 3% and long bonds will approach 3% (while US 10s will once again approach 2%)

p.s. bonus forecast item: Netherlands wins World Cup -- go Orange!

{kind=link}