*** denotes well-worth reading in full at source (even if excerpted extensively here)

Economic and Market Fare:

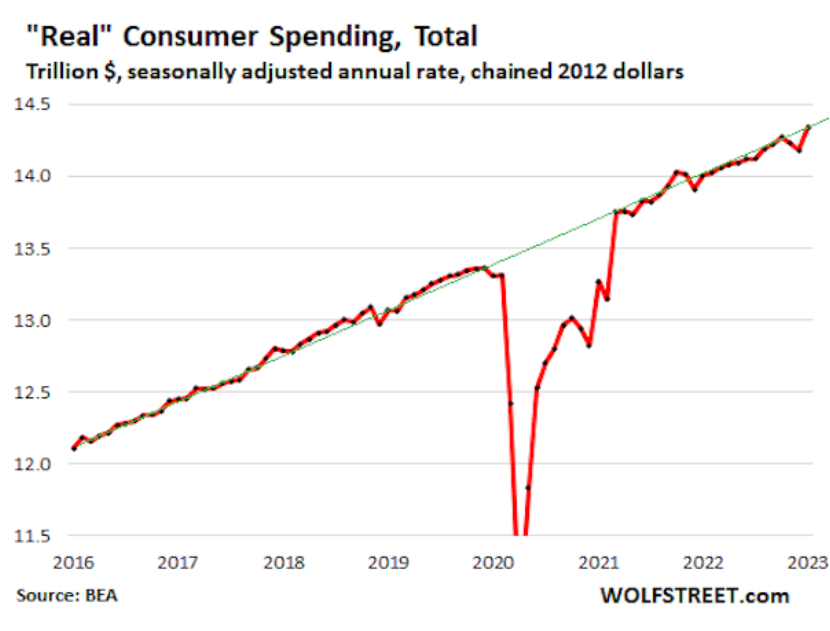

Here's Where The Surge In January Spending And Inflation Came From: Biggest Tax Drop In History

.... So far so good, but what makes historical comps difficult is that in January, there was a comprehensive overhaul of the underlying data. As the BEA notes, "for July through September, estimates for compensation, personal taxes, and contributions for government social insurance reflect the incorporation of updated third-quarter wage and salary data from the Bureau of Labor Statistics Quarterly Census of Employment and Wages program."

Which means that January data was unique in that it was based on revised historical data, while layering on top new numbers for January, which also incorporate several fundamental changes as a result of the new year. .......

Kayfabe: Inflation Idolatry

.... If you have never heard of hedonic adjustments or the substitution effect, the Boskin Commission, or how what I call ‘phoney baloney’ inflation data was institutionalized, then I encourage you to read/revisit that piece.

These concepts are all once again timely, as the recent uptick in reported inflation data appears to have contributed to interest rate markets repricing significantly. Whereas rates markets had priced in a significant probability of the US Federal Reserve reversing course and cutting rates in the 2nd half of 2023 and into 2024, the confluence of hotter than expected inflation reports along with non-farm payroll and retail sales, has largely wiped out those odds and pushed the likelihood of rate cuts out further into the future. .................

............ On a cyclical basis, the rate of consumer inflation has very likely peaked. In addition, barring scenarios such as a severe currency depreciation/crisis, recessions are typically disinflationary/deflationary…..eventually. Markets, and perhaps the Fed, appear caught up in a renewed mini-bout of inflation anxiety and even a theoretical “soft landing” scenario for the US and Eurozone economies. Such bouts of optimism have been pretty normal immediately preceding and/or well into recessionary periods historically, as took place in early 2001 and well into 2008, for example. While the forecast from Kayfabe Capital Tower remains a severe global recession, becoming obvious even to the Fed sometime in 2023, that will eventually cause ‘inflation’ to fall further.

Grannis: Inflation Fears Are Overblown

Stock market bears are fixated on the belief that inflation is not only "running hot" but also "accelerating." Nothing could be further from the truth.

Some charts that help put things into perspective: .......

Conclusion: the Fed should stand pat and watch how things evolve from here. ......

Chart #5 shows that natural gas prices have truly collapsed, falling by way more than ever before in a short span of time. Traders say it's due to warm weather in the East. Regardless, this is an important source of energy for vast swaths of the economy, and it equates to a powerful deflationary force. And let's not forget that oil prices have plunged 35% from their highs last May. It's not just the weather; commodity prices are down across the board over the past 6-12 months. Monetary policy is undoubtedly one of the reasons. .........

Chart #8 shows the year over year changes in the Personal Consumption Deflators (with the Core version being the Fed's favorite measure of inflation). Both rates came in a few tenths of a percent higher than the market expected. Does that sound like inflation accelerating? Or running hot? No. Inflation pressures peaked many months ago. Both of these measures are on track to show year over year gains that are much lower than their current level. It takes time for monetary policy–which is undoubtedly tight—to work its way through the economy. We just need to be patient.

Next Tuesday we'll have the all-important release of the January M2 money supply number. I expect it will show a continued decline, which will strongly reinforce the outlook for slowing inflation in the months to come.

Variant Perception: The Capex Supercycle

An old asset base + large infrastructure spending gap + negative real financing costs (financial repression) = an incoming capex supercycle. This is the final part of our 3-part series based on the insights from our “Age of Scarcity” thematic report sent to VP clients in November 2022. See here for Part 1 and Part 2.

The US’s fixed asset base is extremely old. The last time it was this old was just after WWII, which preceded a huge capex reconstruction boom. The American Society of Civil Engineers has graded the US infrastructure as C-. The Global Infrastructure Hub estimates that the infrastructure spending gap is now at 800bn USD per year (right-hand chart). The surge in net-zero commitments will also necessitate plenty of investment and capex.

Is it finally “infrastructure week”? Minsky called it “managerial welfare-state capitalism”: big government + big business + big labor. Financial repression is usually needed to keep debt servicing costs low. There are lots of successful examples: ......

.... Infrastructure is in the sweet spot of being a politically-favored industry and capital scarce, and is set to benefit greatly out of the next recession.

...... Do not forget about the importance of the business cycle. Liquidity leading indicators lead global listed infrastructure returns (top chart). All of VP’s cyclical indicators point risk-off on a 6-month horizon .......

Jim Chanos, the president and founder of Kynikos Associates and well-known investment manager talks to Rob about the post-pandemic financial system, which has become more steeped in a casino culture than it has been in a very long time, and whether China’s financial situation serves as an example or as a warning.

Bubble Fare:

It took ~15 years but over time retail investors have totally forgotten the pain of 2008. After the 1930s, the generations that endured that pain NEVER forgot, even decades later.

Today's financial media is wholly derelict in their duties, as they have been for decades amid an ever-growing debt bubble heading for inevitable disaster. .....

.... So far, global housing prices - with some regional exceptions - are holding up, but sales volumes have collapsed. A precursor to major price decline.

Archaic perhaps, but I am an impassioned proponent of sound money – and have been for a long time. It’s vital – fundamental. The Austrian School of Economics heavily influences my analytical framework. I focus first on Credit inflation – the expansion of new financial claims. This new purchasing power has varied inflationary effects – including consumer and producer price inflation, asset price inflation and Bubbles, over/mal-investment, trade and current account deficits…

Prolonged periods of excessive Credit growth ensure Bubbles (i.e. Credit, asset, speculative and investment) and progressively destabilizing Monetary Disorder. Inflation is insidious, pernicious and poorly understood. Policy and economic circles will continue to debate “r-star” (the so-called “natural rate” of interest). Others will waste time debating the appropriate inflation target rate. Two or 3% doesn't matter at this point. Decades of damage have been wrought to financial, market and economic structures.

We’re now three decades into history’s greatest Credit Bubble, which, not by accident, coincided with radical monetary management experimentation. I often refer to the “Terminal Phase” of Bubble excess, with systemic risks rising exponentially as the cycle comes to its fateful conclusion. That these dynamics have unfolded on an unprecedented global scale only makes the backdrop more perilous. ..........

Suddenly, it’s as if global markets have awoken to the risk that central bankers might be battling stubborn inflation for several years. What a difference a few weeks make.

I certainly have my doubts that consumer inflation will conveniently return to previous dynamics. New cycle dynamics are at play. Indeed, there is today every reason to expect ongoing deterioration in the geopolitical backdrop. The forces of “de-globalization” and, more specifically, decoupling from Russia and China gain momentum by the week. In the U.S. and elsewhere, there are powerful investment booms associated with domestic manufacturing, renewable energy, infrastructure, defense spending and climate change. And there aren’t enough workers. These are patently not elements of previous cycle dynamics.

.... I expect California to illuminate a fundamental Bubble maxim: inflation may appear the great wealth creator during the boom, but when Bubbles burst the true scope of wealth destruction is revealed. California has plenty of company. Bursting Japanese and Chinese Bubbles, in particular, will expose epic inflated perceived wealth, mal-investment and wealth destruction.

........... I certainly don’t sense that markets are prepared for a return of the 2022 dynamic – only worse. But when deleveraging takes hold, the questions from last year will return: Where is the Fed put? How quickly would the Fed shift to QE – and at what size? And the more persistent inflationary pressures, the more difficult these questions will be for the Fed. At this point, any serious de-risking/deleveraging episode comes with major risks. The day markets begin to question the Fed and global central bank liquidity backstop, there is a serious problem.

A scenario doesn’t seem that far-fetched to me. Confidence in China’s recovery wanes. The new BOJ governor faces a disorderly yen devaluation and fragile bond market. Already destabilized global markets – especially the vulnerable European periphery and EM – get hit by geopolitical developments. Escalation in the Ukraine war – nuclear blackmail. The U.S. responds to Chinese war support with sanctions – China reciprocates. Things become heated. Global markets turn dicey, with pressure on the Fed to intervene with bond market-stabilizing QE. With one eye on shaky markets and the other on sticky inflation, how will the Powell Fed respond? Will it suffice? Years of unsound “money” coming home to roost. ..........

Quotes of the Week:

18/19

— Michael Pettis (@michaelxpettis) February 25, 2023

We have to return to the old, discredited (but highly successful) idea that a more legitimate purpose of economic development is in fact to increase, or at least maintain, the relative share households retain of what they produce.

Charts:

1:

A great chart to highlight how far we are from “landing.” Every landing in stocks and the economy begins with housing.

— Kantro (@MichaelKantro) February 25, 2023

No, we’re not home yet. #macro #Hope https://t.co/jgI3AKy44M

(not just) for the ESG crowd:

As EV batteries consume more lithium, report warns against increased mining of it

Other Fare:

In Indonesia, sickness and pollution plague a sprawling factory complex that supplies the world with crucial battery materials.

.... A decade ago, Labota was a fishing village; today it’s been subsumed into a sprawling city centered around IMIP, a $15 billion, 3,000-hectare industrial complex containing steelworks, coal power plants, and manganese processors, with its own airport and seaport. Built as a joint venture between Chinese and Indonesian industrial companies, it is at the heart of Indonesia’s push to supply the electric vehicle market with nickel, a core component of batteries.

Rocketing demand for electric vehicles, combined with supply disruptions caused by Russia’s invasion of Ukraine, have made Indonesia—and IMIP—a critical link in the supply chains of EV manufacturers. That's especially true for Tesla, which has signed multibillion-dollar deals with companies at the site and is reportedly in talks to set up its own manufacturing facility in the Southeast Asian country.

Meeting this demand has come at a huge social and environmental cost. ........

In this issue: ▸ ESG ratings both wrong and scary ▸ Executives get “green” bonuses despite slow progress ▸ The US will make “no apologies” for green jobs ▸ And much more...

...... There is something scary, very scary about this. ESG is becoming a tool that upholds the system of the 10%. It is not and never was the intention of ESG. The current ESG ratings provided to the financial markets are simply not only wrong, they are also not really helping us to develop the markets and companies where ESG measures would most likely make the biggest difference.

Other Fare:

On Perry Mehrling’s “Money and Empire: Charles P. Kindleberger and the Dollar System”

Pics of the Week: