The current bounce in equity markets from October continues to outpace historical rallies in bear markets, bolstering the case that the low may be in for this cycle.

It always pays to remember that the path of least resistance for stock markets is up. Bear markets are the exception, not the rule, but they are, as Thomas Hobbes described life without government, “nasty, brutish and short”.

While the current bear market is longer than most, it is still nonetheless a risk for investors wondering whether the current rally is really the beginning of the end of the downturn, or merely the prelude to a nasty sell-off ahead, with new lows plumbed.

No-one knows for sure of course, but the current rally has remained more robust than perhaps most would have expected. ... As the chart below shows, the S&P is diverging further away from historical bear-market rallies.

Firms that use computers to determine buy and sell signals have been loading up while other investors sit back

The US has its market leading "Big 7 Tech" basket (a play on AI hype but really just an excuse to buy the former market leaders Apple, Microsoft, Google, Amazon, Nvidia, Meta, Tesla), which is trading on 30x PE vs 17x for rest of S&P and is single-handedly responsible for all market gains in 2023; Europe on the other hand, has its "Big 7 European Luxury" aspirational basket (LVMH, L'Oreal, Hermes, Christian Dior, Richemont, Kering, Ferrari) which is trading at an even more ridiculous 36x vs rest of Stoxx 600 trading on 12x PE.

..... As BofA's Michael Hartnett discussed over the weekend, in the past year this high-flying sector had become to European stocks what Big Tech was to the US: a collection of dominant businesses whose explosive growth was unquestioned even as the economy shrank. But the questions are finally starting to emerge as confidence in that view has been dented ...

Despite the stock market rally so far in 2023, the S&P 500 Index has not come close to regaining its all-time high put in early last year.

What has soared to new highs, however, is the stock/bond ratio.

In fact, its ascent has been so strong that, over the past two decades, the SPY-to-TLT ratio has only been as overbought (as measured by quarterly RSI) as it is today at the 2007 top heading into the GFC.

...Zeitgeist I: “I mean, if you're going to lose your job and be replaced by AI in the next few years, might as well own some AI as a hedge, no?"

Zeitgeist II: “Bubbles not easy, put plenty of investors out of business. But this one you getting paid by fat yields in cash & bonds to ignore for now. Why no FOMO yet.”

Zeitgeist III: “4% real yields popped internet bubble, 3% popped subprime, crypto crashed on real yield rip from -100bps to 150bps. But market telling you real rates may need to rise another 100-150 bps from here to pop ‘baby bubble’ in AI.”

The yield-curve model developed by a former colleague at the New York Fed has been a reliable indicator that a recession was brewing just over the horizon (with that horizon being about one year) but the model is an indicator model not a causal one. A second indicator for us is the share of profits in GDP (we use the nonfinancial corporate sector for both measures) and we view this as a causal model. Declining profitability causes companies to cut back on hiring and investment to restore profitability and conserve cash but this in turn kicks in the Keynesian multiplier from capital spending to GDP growth and disrupts the circular flow of income—eventually leading to a downturn in consumer spending. Every recession has been preceded by a squeeze in profit margins (technically the 1981-82 recession was not but this was because the path of growth was disrupted by the imposition and then removal of credit controls that induced a short recession in 1980). With the revision to first-quarter GDP, yesterday’s data showed a second consecutive quarterly decline in profit margins. Nonfinancial domestic corporate profit margins have now contracted from a peak of 16.3% in the second quarter of 2021 to 14.6% in the first quarter of this year—a decline that is sufficiently large to constitute a solid signal that a recession is likely looming.

The one caveat that is worth making is that the nonfinancial corporate GDP data, which are derived from incomes and profits, show a very weak picture of the economy already. Real output for this sector has declined in four of the last five quarters which has never occurred with the economy not already in recession. However, private nonfinancial payrolls have risen at an annualized pace of 3.7% over these same five quarters, which has typically suggested that the economy was still in the expansion phase. Why would companies experiencing declining output volumes grow employment at a fairly rapid clip? We believe it is easier to count heads than measure real output and strong job growth in 2022 was just reaffirmed by the latest QCEW data (which is based on state-level unemployment insurance accounting). Nonetheless, with an inverted yield curve and profit margins declining, the probability of a recession beginning later in 2023 or early 2024 has surely increased.

............ It is important not to be Pollyannish about the economy’s near-term prospects. Under almost any scenario, they will be difficult. GDP growth will halt, employment gains will come to a standstill, and unemployment will push higher. However, while history suggests that high inflation and an aggressive Fed mean recession is a serious threat, this time is different enough for the economy that a recession is avoidable. In my more than 30 years as a professional economist, I have never seen such recession pessimism. But I have also never seen such a resilient economy. Something has to give. I suspect it will be the pessimists.

In the FOMC's efforts to bring down inflation, the Committee has not been shy about the need for policy to turn restrictive. Determining the level of interest rates which adequately weighs on activity and thereby inflation without causing untoward damage to the economy is by no means easy, but is important when the effects of policy changes are not immediately felt across the economy.

One guidepost policymakers use in this endeavor is the natural rate of interest, or r-star. R-star can be thought of as the real short-term interest rate that prevails when the economy is expanding at its potential rate and inflation is stable. In cannot be directly measured, but is rather inferred from how other parts of the economy act in relation to each other. As relationships between real GDP, inflation and the federal funds rate change, so do estimates of r-star. For example, after vacillating from about 2.5%-4.0% from the mid-1980s to early 2000s, the estimated natural rate of interest fell to less than 1% following the 2008 financial crisis (chart).

The extreme volatility in data following the economy's abrupt shutdowns in 2020 and subsequent reopening made it particularly difficult to extract r-star. The most widely-followed estimates, published by the New York Fed, were temporarily halted while researchers made adjustments to the models after such extraordinary shocks but have resumed this month.

Since the COVID-19 pandemic, r-star seems to have been little changed. Over the past four quarters, the Holston-LaubachWilliams model estimated the U.S. natural rate of interest averaged 0.76%, nearly spot on the pre-pandemic five-year average of 0.77%. In other words, it appears that through all the tumult of the past few years, the era of a low natural rate of interest is ongoing. That may seem surprising given the recent degree of inflation, but comes as potential output is estimated to have been reduced by a whopping 4% relative to its pre-pandemic projection.

The prevailing low rate of r-star suggests that the FOMC does not have to raise the nominal fed funds rate as far above inflation to rein in price growth as in prior cycles when the natural rate of interest was higher. However, even when accounting for the current environment's low rate of r-star, policy still has yet to clearly become restrictive, given the underlying strength of inflation (chart). That does not necessarily entail that the FOMC hikes further from here, but it does suggest that if Fed officials do indeed believe policy needs to be restrictive for a time, inflation needs to ease very soon.

The economy continues to decelerate, and the most recent data adds significant evidence to the possibility the economy entered a recession last year or at the start of this year. While a recession may already be underway, the deterioration in the labor market has not proven sufficient for the Federal Reserve to soften its continued hawkish policy stance.

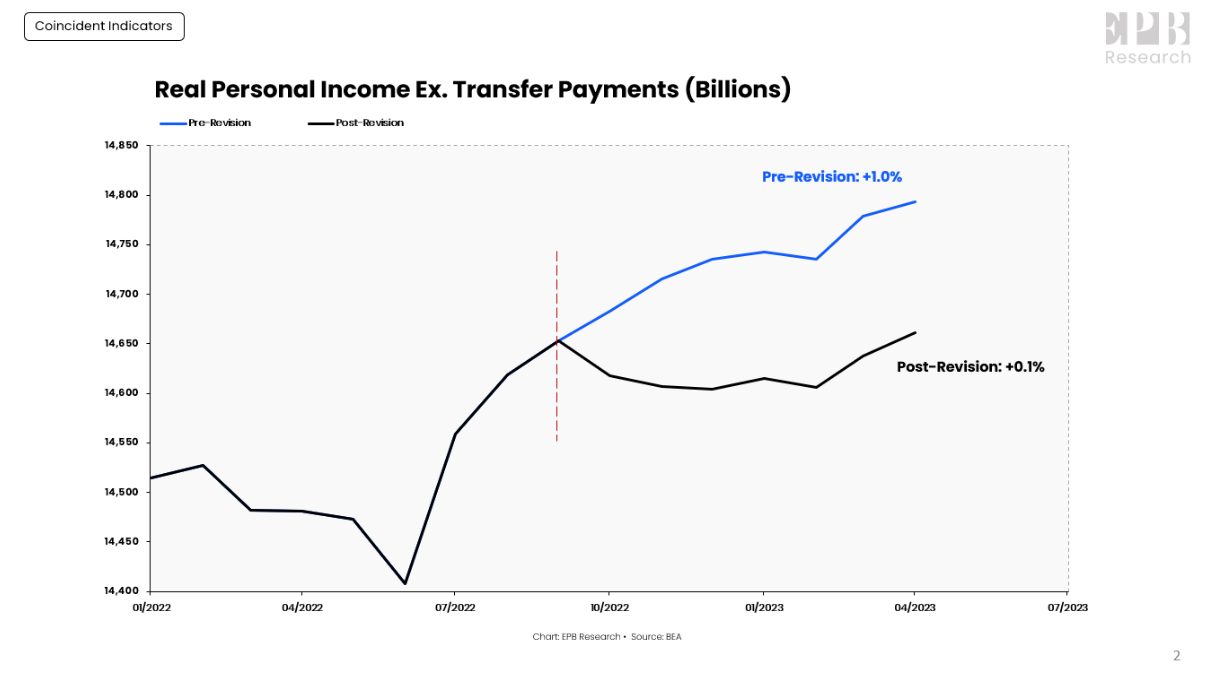

In this update, we’ll review the changes and revisions to coincident economic data and zoom in on the initial jobless claims data, which will be our most real-time and reliable labor market measure.

The Bureau of Economic Analysis recently reported the April update for Personal Income and Personal Consumption. The BEA significantly revised the Personal Income data from September 2022 through March 2023.

Real personal income less transfer payments, our preferred income metric, only posted a 0.1% gain since September of last year compared to a previously thought 1.0%. .......

No comments:

Post a Comment