***** denotes well-worth reading in full at source (even if excerpted extensively here)

Economic and Market Fare:

In my economic slowdown post a month ago I was generally upbeat, but I worried about the slowdown in job creation. Those worries faded with a strong January jobs number. The US economy is ok: credit spreads are still quite low, liquidity is still abundant, the dollar is still strong, inflation is still declining, and there are only a few indicators that suggest caution. ......

US money market fund assets hit a record high of $6trln this week. Gov’t debt hit record highs too. As did US equities, in general. Gold is near a record, US home prices too. In a highly financialized fiat monetary system, many drivers work to influence valuations. Cash flows, earnings, leverage, interest rates, money supply, its velocity, tax rates, optimism, pessimism, uncertainty, confidence, stability, volatility, and expectations about how all such things will change. Investors search for fair market value, but for a trader there’s no such thing, only price.

Money can be created in all sorts of ways in a fiat monetary system. This makes it hard to know how much there is at any given point in time. And while it makes sense that the more money lying around, the higher prices should be in the system. But sometimes, money changes hands slowly, and when this happens, prices can actually move lower no matter how much money is in the system. The inverse is also true. And this makes it even harder to determine the fair value of anything, because it requires you to have to anticipate the velocity of money.

There are periods during which the relationship between most or all the variables that investors use to determine fair value remain rather stable. Those are fairly boring times, and the people who profit the most engage in leveraged carry and mean-reversion types of strategies. Such periods give investors a false sense of confidence that market prices can be forecasted with great confidence using a range of inputs. As confidence turns to arrogance, the potential energy for a major market shift builds. Investors get short volatility. This dynamic never changes.

The equity risk premium (ERP) is at 23-year lows. The S&P 500 earnings yield minus 3mth T-bill yields has not been this low since 2001. So, in at least one sense, the market is above fair value. But at the height of the dotcom bubble, the ERP was lower than now. So, all this tells us is that the market is overvalued, and we should not be surprised to see it become more so. No one knows whether the dotcom ERP lows represent an absolute limit. All we know from the past is that when markets move to extreme over/under-valuations, wild moves in price can happen. .....

New highs exceeding new lows creates a favorable risk/reward environment and other takeaways from the week

..... Rather than being overly concerned about breadth weakening, our work indicates that bull market behavior is persisting. In such an environment it makes sense to see the Dow Transports (and the Transportation ETF) breaking through resistance and RSP (the equal-weight S&P 500 ETF) moving to a new all-time high.

While the week is not in the books just year, we are on the cusp of five consecutive weekly gains of 1% or more for the S&P 500. This has only happened 11 times in the past three-quarters of a century (most recently in late-2016 and mid-2009).

***** Hussman: Cluster of Woe

......... Our most reliable valuation measures are again beyond every extreme in U.S. history prior to March 2021, apart from 5 weeks surrounding the 1929 market peak. Meanwhile, our most reliable gauge of market internals remains unfavorable as the result of persistent divergences across individual securities and sectors. Yet even though the market has lagged Treasury bills for more than two years, my impression is that investors feel an almost excruciating “fear of missing out” amid nominal record highs in the S&P 500 and Nasdaq 100, enthusiasm about an economic “soft landing,” and an expected “pivot” to lower interest rates. In my view, abandoning systematic investment discipline amid the most extreme market conditions in history would be a costly way to buy a fleeting sigh of relief.

We know that valuations are informative about long-term returns and full-cycle losses, but not about short-term outcomes. The only way the market could reach valuations as extreme as today was to advance, unfazed, through every lesser extreme. So it’s not just extreme valuations, but the full combination of extreme valuations, divergent market internals, and a fresh preponderance of warning flags that holds us to a defensive outlook here. ..........

..... On the subject of corporate earnings, it’s worth repeating that the surplus of one sector of the economy (income in excess of consumption and net investment) is always the deficit of other sectors (government, households, and foreign trading partners). That’s not a theory, it’s just an accounting identity. Nothing – not monetary policy, not debt creation, not bank lending – nothing changes the arithmetic. It’s just math.

When investors look at current record profit margins and corporate free cash flow, they should recognize that this apparent prosperity is possible only because of massive deficits in the government sector, and depressed savings in the household sector in recent years. Sustaining one requires sustaining the other. Again, that’s not a theory, it’s just arithmetic. ..... The key point is simple: the “prosperity” of U.S. corporations here is the mirror image of massive government deficits and weak household savings. ........

Recession risk is still present

Amid the enthusiasm and now nearly unanimous consensus that recession risk is behind us, I’ll reiterate our own view: the data remain consistent with a U.S. economy at the borderline of recession, but we would need more evidence to expect that outcome with confidence. ........

...

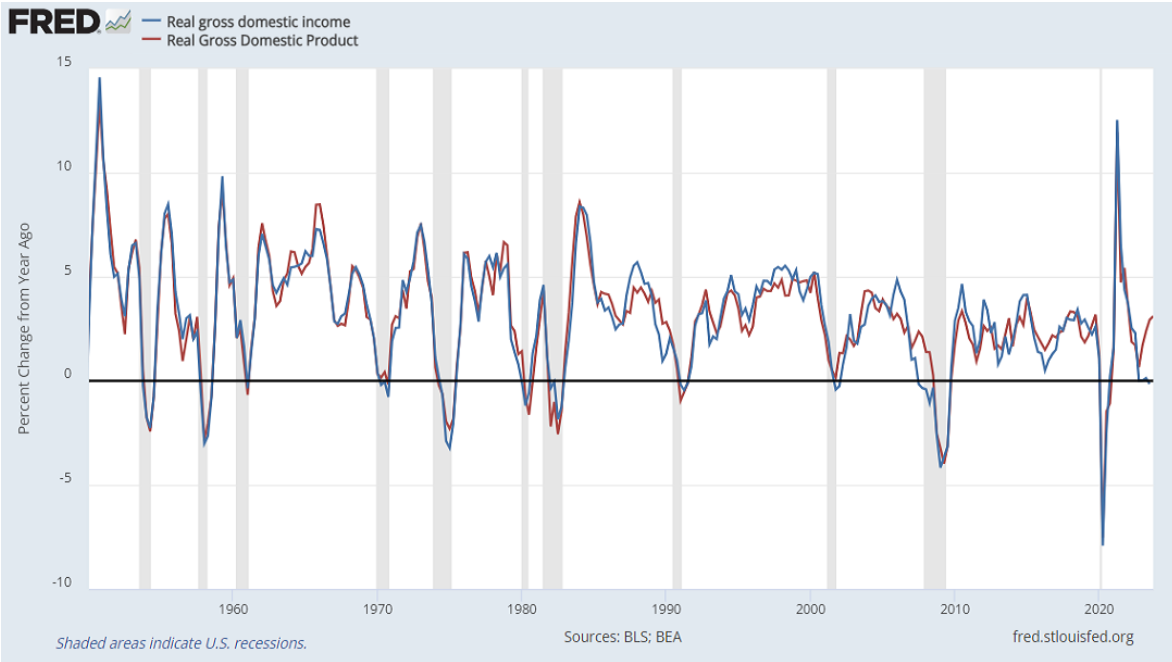

......... Two additional disparities are worth monitoring. The chart below shows the year-over-year growth of real Gross Domestic Income versus real Gross Domestic Product. Technically, these measure the same thing, just in different ways, and they’re normally identical aside from a small statistical disparity. In a few cases, however, as when the U.S. was rolling into global financial crisis, GDI fell into contraction well before GDP. Currently, GDI is again in contraction year-over-year, making it difficult to take the robust 4th quarter GDP figures at face value. It may be best to allow the possibility that a “soft landing” may not be as sure as it seems.

We observe a similar disparity in job surveys that also measure the same thing in different ways. In this case, job growth as measured by the “household survey,” which delivers the unemployment rate, has been markedly weaker than the “establishment survey,” which delivers the “headline” jobs number. Here, the household survey is clearly more volatile. Because it’s not as heavily “smoothed,” quick swings can sometimes be informative about emerging trends, but those swings can also represent noise.

As with all noise reduction problems, it’s best to draw information by combining multiple sensors. In the context of weakening order surplus, employment composition, and GDI, the weak job creation in the household sector contributes to our view that recession concerns shouldn’t be easily dismissed.

Executive Summary

The S&P 500 has become an increasingly concentrated index over the past decade, with the top seven stocks now comprising 28% of the total, and the returns of those stocks far outpacing that of the average stock in the index. Active managers are systematically underweight the very largest stocks, and this is particularly true of concentrated high active share managers. If the purpose of a benchmark is to be a fair measuring stick to determine whether a manager has skill, a market capitalization-weighted index is not a good benchmark for most active managers, and this becomes increasingly true as the index becomes more concentrated. History suggests that the next decade is likely to see a reversal of the recent pattern with the capitalization-weighted version of the S&P 500 underperforming the equal-weighted version. In such an environment, active managers will suddenly look much better versus the S&P 500 and other capitalization-weighted benchmarks.

Patience is widely understood to be a virtue in investing. Many clients and investment committees pride themselves on their willingness to stick with high conviction managers through rough patches in performance in the belief that given sufficient time, skill will tell. But even patient investors have their limits, and this fall we saw an avalanche of questions coming in from institutions as to whether it is time to abandon active management, at least in U.S. large caps. We were a little surprised by this, since our U.S. large cap equity products have actually done well against their benchmarks over the last few years. 1 But a little digging made us realize that most clients’ experience with their active U.S. equity strategies has been pretty disappointing. According to Morningstar, 74% of U.S. large cap blend managers underperformed the S&P 500 last year. And it wasn’t just a single bad year. The decade ending in 2023 saw a stunning 90.2% of U.S. large cap blend managers underperform their benchmarks ...........

......... The largest stocks generally become the largest by way of becoming expensive, and this anti-value tilt has historically been quite costly, explaining most of these companies’ poor relative returns. 6 Good returns in the face of high valuations, moreover, require exceptional earnings growth. When a company already has a substantial market and profit share of the industries in which it operates, unusual growth tends to be significantly harder than normal. ....... Since 1957, the 10 largest stocks in the S&P 500 have underperformed an equal-weighted index of the remaining 490 stocks by 2.4% per year. But the last decade has been a very notable departure from that trend, with the largest 10 outperforming by a massive 4.9% per year on average. .........

The U.S. corporate bond market is set to break new issuance records as borrowers take advantage of lower financing costs than last year and investors, emboldened by the prospect of an economic "soft landing," pile into the asset class. ...

Issuance of bonds by companies rated investment-grade surged above $196 billion last month, making it the busiest January on record. This record issuance may be repeated this month, with BofA Global estimating nearly $160 billion to $170 billion in just investment-grade rated bond supply, which would make it the busiest February ever. ....

Sponsors under pressure from investors to return cash but are finding it harder to offload companies

......... Corporate borrowers sold $8.1bn worth of junk-rated US loans to fund payments to shareholders in January, more than six times December’s total and the highest monthly figure in more than two years. Most were issued by companies backed by private equity firms, according to data from PitchBook LCD.

With weak deal volumes and sluggish demand for initial public offerings making it harder to offload existing investments, private equity firms are turning to such so-called dividend recapitalisations to pacify investors eager for a return on their capital. ...

Coopting Disruption

Our economy is dominated by five aging tech giants – Alphabet, Amazon, Apple, Meta, and Microsoft. In the last twenty years, no company has commercialized a new technology in a way that threatens them. Why?

We argue that the tech giants have learned how to coopt disruption. They identify potentially disruptive technologies, use their money to influence the startups developing them, strategically dole out access to the resources the startups need to grow, and seek regulation that makes it harder for the startups to compete. When a threat emerges, they buy it off. And after they acquire a startup, they redirect its people and assets to their own innovation needs. These seemingly unrelated behaviors work together to enable the tech giants to maintain their dominance in the face of disruptive innovations.

Quotes of the Week:

...

...

...

...

...

(not just) for the ESG crowd:

Summer Has Long Stressed Electric Grids. Now Winter Does, Too.

........... U.S. grids are also struggling because they are importing less power during the winter from Canada. Demand for electricity in that country is growing strongly, and a decline in rain and snow has reduced supply from its hydroelectric power plants .........

Is the popular energy transition narrative valid or is it imaginary?

The world used almost 180,000 terawatt hours of primary energy in 2022. Less than 5% of that was from wind and solar. That’s not a lot to show for total investment in renewable energy of more than $16 trillion over the last twenty years.

..... Since the strong regulations on sulfur pollution from ships went into effect in 2020, solar radiation absorbed by Earth has increased about 3 Watts per meter squared in the North Pacific and North Atlantic. Commercial shipping, it turns out, had been geoengineering a cooler planet by pumping sulfur dioxide into the lower atmosphere, reflecting sunlight back to space. Contrails do that too, only higher up. When ship emissions suddenly stopped, what occurred was exactly what the anti-geoengineers have been warning us about — termination shock. The same happened in the days following 9–11 when air traffic was grounded over North America. If you don’t yet believe aerosol reduction contributed to the weather extremes the world witnessed in 2023 (and many well-informed scientists still don’t), just wait because maritime regulations are doubling down in 2024, and AI-assisted greening of air travel will also start to curtail contrails. ...........

In their 2024 NASA paper, “Global Warming in the Pipeline,” NASA’s James Hansen, Leon Simons and a dozen other prominent scientists indicated that 4.8°C warming is already baked in the cake. It’s been masked by aerosols. Take away the aerosols and voila! With sulfur rules in place, we blew through the Paris target of 1.5°C in 2023 and now have 2°C in our sights. Hansen told a UN network interviewer, Jeffrey Sachs:

You’re still getting some warming from additions to the imbalance that occurred 100 years ago but as we show quantitatively in the paper, [we can] expect at least a 50% increase in the warming rate and that’s what we will we will soon find out.

***

You know one Watt per meter squared is an enormous forcing to try to overcome. I mentioned that if you want to do it by extracting CO2 it costs you more than a hundred trillion dollars. It’s not going to happen. So young people need to understand what they are being handed by the older generations.

Geopolitical Fare:

... Whatever you think of Putin, at least he’s educated and speak in complete sentences and has a historical understanding (whether you agree with it or not.) He makes Trump and Biden look like the idiots they are.

In fact, Putin makes almost every Western leader look like an ill-educated moron. Orban is an exception. This isn’t a political judgment. I don’t much like Putin, but I can respect him. I can’t respect Biden, Trump, Sunak, Scholz, Macron, Von Der Leyen or my own PM, Trudeau. .........

This Putin/Carlson interview is super embarassing to the West. I literally can’t think of a Western leader today who could lay out a case like this, coherently and intelligently. We are ruled by imbeciles. ........

One of the noblest and most important things a western journalist can do these days is help expose the propagandistic manipulations of the mainstream western press institutions who have duped our civilization into consenting to a profoundly dysfunctional status quo which does not serve the interests of normal human beings. Unfortunately this rarely happens, because western journalists tend to view the mainstream press as allies and potential employers.

This happens to be one such rare occasion, and it happened in one of the last places you’d probably have guessed if you follow mass media propaganda with a critical eye. The Guardian has a great new article out titled “CNN staff say network’s pro-Israel slant amounts to ‘journalistic malpractice’” by a guy named Chris McGreal which cites multiple CNN staff members and internal documents to reveal the immense top-down pressure in the network to tilt coverage heavily in favor of Israel. .........

Our world will never see the revolutionary changes it desperately needs until the people begin using the power of their numbers to force those changes to happen, and the people will never start using the power of their numbers to force revolutionary change as long as they are being manipulated by propagandists into accepting the status quo. Our task therefore, as people who love truth and desire a healthy world, is to begin waking the public up to the reality that everything they’ve been told about their society, their government and their world is a lie, and pointing them toward true information about what’s really going on. ....

..... Do you realize the danger of exposing Americans to what this Putin might say? Hearing him express his thoughts about the world situation in a leisurely format — which Putin does regularly among his own people (I’ve seen him do it!) — is liable to inform Americans that their own political leadership is a party of mental illness.

........ The president is, after all, nothing but a simulacrum or figurehead of power. The real power is invested in his representatives, who represent the corporations and billionaires who own the place.

......... This is the Old Boys Club, of which Biden has been a proud member iin good standing for nearly half a century!

Other Fare:

The How Of Why: Not Quite A Review (Part II)

.... Goff’s ultimate conclusion should be attractive to many: rather than being thrown by mere random chance into the cold and uncaring void of the universe, to live out a brief, confused existence and then wink out into the nothingness whence we came, the existence of complex life in the world is due to a larger purpose, an overall arc that bends into the direction of greater objective value. Moreover, rather than going the traditional route and appealing to some omniscient, omnipotent, and omnibenevolent creator God that sees to it that everything unfolds according to His divine (and commonly, unfathomable) design, he proposes a way to reap those benefits without all the boring Sunday prayer sessions!

Thus, he breaks largely untrodden ground: proposing a middle way between a scientific, materialist, but ultimately uncaring cosmos, and a world unfolding according to a divine, but irreducibly mysterious, purpose. Just as evolution can give us design without a designer, he proposes meaning without a meaner. If this were a religion, I could well see myself signing up for it—but since it’s not, I don’t even have to do that! However, as also hinted at in the last column, the more alluring the conclusion, the more we have to critically examine the arguments leading up to it. ......

Pics of the Week:

No comments:

Post a Comment