*** denotes well-worth reading in full at source (even if excerpted extensively here)

Economic and Market Fare:

Seth Klarman outlines the lessons that investors were quick to forget only two years following one of the greatest financial meltdowns in modern history.

........ Each new generation of investors suffers from involuntary amnesia; not being blessed with the scars from volatile periods in the market like their more tenured peers. I was not an investor during the GFC. Despite reading about it at length, I will never have the “benefit” of knowing what that felt like. These moments, while at times costly (both to your asset values and pride) are supposed to shape you; to make you a better investor for the decades to come. If you are fortunate enough to be young, then the lessons won’t appear so expensive further down the line. But the worst outcome is the investor who does experience something and learns nothing from it; voluntary amnesia. ......

Twenty Investment Lessons of 2008

1. Things that have never happened before are bound to occur with some regularity. You must always be prepared for the unexpected, including sudden, sharp downward swings in markets and the economy. Whatever adverse scenario you can contemplate, reality can be far worse.

...

4. Risk is not inherent in an investment; it is always relative to the price paid. Uncertainty is not the same as risk. Indeed, when great uncertainty – such as in the fall of 2008 – drives securities prices to especially low levels, they often become less risky investments.

......

7. The latest trade of a security creates a dangerous illusion that its market price approximates its true value. This mirage is especially dangerous during periods of market exuberance. The concept of “private market value” as an anchor to the proper valuation of a business can also be greatly skewed during ebullient times and should always be considered with a healthy degree of scepticism.

.......

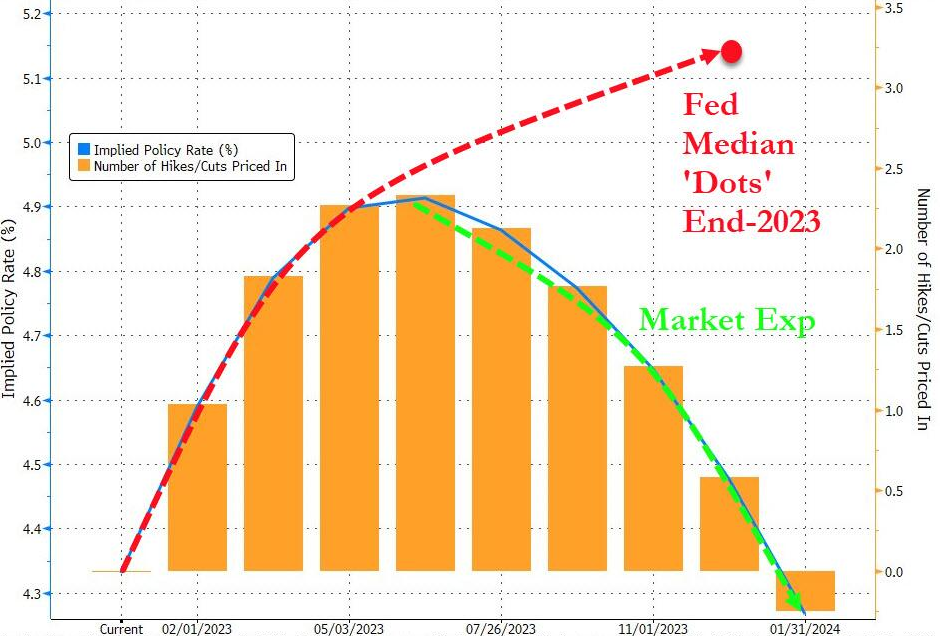

Tl;dr: The Fed hiked 25bps as fully expected and the statement had 3 key highlights:

- Hawkish - keeps "ongoing increases" (plural) language signaling no pause in March.

- Small Dovish - adds inflation "has eased somewhat" but notes "remains elevated."

- Dovish - Changes "pace" of future increases with "extent", as it transitions from the rate of hikes to the duration of higher rates before any pivot.

.....

Tl;dr: Markets melted up after the following folding foursome:

- Fed's Powell says "disinflation" 13 times

- BOC pausing

- BOE pausing

- ECB one more and done, turns to "climate QE"

Chinese spy balloons floating over the United States. Interest rates at 5%. The economy in full collapse. Inflation at 6%. We'll send you a postcard - everything's fine!

Ultimately, I was proven right in my prognostication when the market crashed in March, before the Fed came in and launched unlimited quantitative easing and the public started to wrap their head around the fact that Covid wasn’t necessarily a death sentence.

Current markets seem hell-bent not just on once again ignoring the obvious right now, but spitting the obvious back in the faces of those who use reality as a guide to their decision making. And the real kick in the nuts is that the Fed, the broadest influencer of our economy and market sentiment, isn’t even a tailwind this time. On the contrary, it is a massive headwind.

The market is simply still hanging around - like a Mortal Kombat character stunned, but still on his feet, waiting for the Fed to deliver the final blow. Old habits die hard. As I pointed out many times just over the last several weeks, it is difficult to break the psychology of market participants who have been conditioned to buy the dip without consequence for the last 15 years. So, in that respect, I’m not surprised the market is rallying despite economic reality. But to say that the market has been grasping for straws when it comes to reasons to rally would be a vast understatement. Take this week for instance. ......

....... I’ll spare you guys the lecture about how 5% interest rates are eventually going to cause the economy to implode. I’ve prattled on about this way too much and continue to believe that it’ll be the case, and that it’s only a matter of time. Let’s only take a look at what’s new. .........

...... When it’s too late, the market will finally get it. This is what happened with Covid in February 2020, this is what happened when Lehman Brothers went under and the housing market crashed and this is what happened leading up to the tech bubble crash in the 2000s.

Markets never crash as warning beacons are making their way out. In the case of the housing market, the market didn’t crash when delinquencies started to tick higher, it just ignored it. In the case of the Covid crash, the market didn’t crash based on the news that Covid cases were spreading in the U.S., it just ignored it. In both cases, the market crashed once the the public was forced to confront the reality of what was happening, and I don’t expect 2023 to be any different. ....

***** Lessons from History

What can the past tell us about today's economy?

History does not repeat, but it rhymes. It is the reflection of human behavioral traits which remain constant over time, with greed and fear the most prominent

As the world economy stands on the cusp of a recession (see last week’s post), it is worthwhile to compare how these unfolded in the past, with similar patterns likely repeated today

This post reviews the past five US recessions, with a particular focus on real disposable income. This economic metric describes nothing but what people have left in their pocket once inflation is deducted. Today, with inflation seemingly on the way out, real income has increased. This lead many, from the FT to Goldman Sachs, to believe a re-acceleration of the economy is on the horizon

History shows that this conclusion is likely wrong, with higher real income in fact a hallmark of recessionary periods. Today’s post explains why this is the case, and highlights some further similarities between past recessions and today

As always, the post concludes with an outlook on current markets. Right now, there is a yawning gap between economic reality and what capital markets price in. I expect this gap to close, with the bond market in the lead and equities soon to follow, and am positioned for it with long bonds and short cyclical equities. .........

.......... Some further interesting commonalities stand out

- Four out of five recessions saw monetary tightening in their runup (Covid-19 the exemption)

- Three recessions saw a prior squeeze in energy costs (1981, 1990, 2008)

- Three recessions saw a bubble burst (1990, 2001, 2008)

- None of these drivers were present in the “false alarms” since the Great Financial Crisis (‘11,’16,’19) when a recession each time was avoided

Today’s economy combines all three drivers - (1) a prior squeeze in energy costs due to Covid-19/ESG/Ukraine, (2) severe monetary tightening as the Fed raised rates from 0 to 4.75% and (3) a burst bubble, in this case housing and Tech

Now, all past five recessions had one dynamic in common: job losses. This brings us back to the central question for this cycle - will unemployment increase?

I’ve already made the case in my last two posts that this is unfortunately, likely the case, despite the various employment tailwinds such as Boomer mass retirements. The evidence has hardened further since. .........

Rather than the 1970s, the post-WWII period may provide a better analogy to today. Public debt was comparably high and the late 1940s shaped by a inflation-deflation-inflation yo-yo ......

***** Parsimonious Put

From Greenspan to Powell

........... But what is the “put,” really? The intent certainly exists for the Fed to act, and potentially in major ways, in order to attempt to buttress the financial system and economy. However, is it pre-ordained to be effective?

What history suggests is that the relative effectiveness of the put correlates with whether or not its timing occurred during a growth rate cycle slowdown, or whether the reflexive forces of business cycle contraction are triggered. This is why a robust business cycle analytical framework is of paramount importance at present, in my opinion..

The theoretical window for a Fed put to be effective would have been when a growth rate cycle slowdown was still plausible. Instead, because of the recent cost of living crisis, the Fed has been tightening through that window!

Broad measures of coincident economic activity for the US have already reached the zero bound, with leading indicators still pointing towards recession. Soft landings have occurred when leading indicators turn back higher without coincident data turning negative.

Despite the backdrop of near-zero growth, the Fed just raised rates once again and hinted at possibly two more 25 bps hikes between now and May. But even if the Fed pauses, that will transpire with recessionary forces likely already being unleashed, and leaving the Fed’s eventual response having to be the opposite of parsimonious in efforts to combat recessionary dynamics. ....

... But, as Statista's Felix Richter notes, that’s not to say the outlook is rosy, as the global economy still faces major headwinds.

Three of the major central banks met and raised their policy interest rates yet again in the so-called ‘fight against inflation’. Interest-rate levels are now at 15-year highs. But the financial markets took the comments of the central bankers as signalling that their policies were working and inflation was falling. And it would fall sufficiently for the central banks to stop raising rates soon and so avoid an economic slump.

This is wishful thinking. The bank chiefs made much of the apparently less worse levels of economic activity in recent real GDP data. But this again is wishful thinking or white-washing. ....

......

Vid Fare:

Quotes of the Week:

Charts:

1: 2:

2:

3: 4:

4:  5:

5:

6:

6:  7:

7:  8:

8:

9:11:

(not just) for the ESG crowd:

However, the IMF predicts the slowdown to be less pronounced than previously anticipated. ...

Roberts: Central banks: boom or slump?

This is wishful thinking. The bank chiefs made much of the apparently less worse levels of economic activity in recent real GDP data. But this again is wishful thinking or white-washing. ....

Despite mounting evidence supporting recession forecasts, the stock market remains at odds with that outlook. Such leaves investors in a predicament of avoiding a further drawdown in the equity markets but not wanting to miss out on a potential recovery.

It is hard to argue with the recession forecasts that currently proliferate the headlines. For example, this excellent piece from Simon White from Bloombergmakes an important observation.

“Stocks will be unable to post a durable rally and exit their bear market until the cycle turns. As the chart below shows, it’s not until leading data start to outperform coincident data once more that stocks turn up.Unfortunately, when leading data are as depressed as they are today relative to coincident data, the cycle does not turn without there being a recession. Based on the historical data, stocks have another 15% or so downside if the US has a recession.”

..... The Leading Economic Index is a significant indicator. In particular, we monitor the 6-month ROC in the Index as it highly correlates to corporate earnings and has a perfect track record in forecasting recessions. Both the 6-month ROC in the LEI and our broad Economic Composite Index (more than 100 individual data points) suggest a recession is imminent.

US Job Opening Far Lower Than Reported By Department Of Labor, UBS Finds

............ Of course, such a high level of job openings is alarming to the Fed for the simple reason that it means Powell has failed at his mission at cooling off what appears to be a red hot jobs market; no wonder the Fed Chair has frequently flagged the high level of job openings as a sign of ongoing strength in the labor market. The bottom line, as UBS notes, is that "the BLS measure, although it has declined, remains historically high."

However, as in the abovementioned case of unexpectedly low jobless claims, there may be more here than meets the eye. According to Villanueva, "a range of other measures of job openings suggest normalization in the labor market—softening much more convincingly, often to pre-pandemic levels" - translation: whether on purpose or accidentally, the BLS is fabricating data. Also, the UBS economist flags, job openings are not a great indicator of current labor market conditions—they lagged the last two downturns in the labor market.

So what's the real story?

Well, as usual there is BLS "data" and everyone else... and as UBS cautions, other measures of openings tell a very different story: "Our UBS Evidence Lab data on job listings is weekly and more timely than the BLS series. The last datapoint is for the week of December 31. It shows openings down 30% from the March 2022 peak and only 25% higher than the 2019 average."

............ Of course, such a high level of job openings is alarming to the Fed for the simple reason that it means Powell has failed at his mission at cooling off what appears to be a red hot jobs market; no wonder the Fed Chair has frequently flagged the high level of job openings as a sign of ongoing strength in the labor market. The bottom line, as UBS notes, is that "the BLS measure, although it has declined, remains historically high."

However, as in the abovementioned case of unexpectedly low jobless claims, there may be more here than meets the eye. According to Villanueva, "a range of other measures of job openings suggest normalization in the labor market—softening much more convincingly, often to pre-pandemic levels" - translation: whether on purpose or accidentally, the BLS is fabricating data. Also, the UBS economist flags, job openings are not a great indicator of current labor market conditions—they lagged the last two downturns in the labor market.

So what's the real story?

Well, as usual there is BLS "data" and everyone else... and as UBS cautions, other measures of openings tell a very different story: "Our UBS Evidence Lab data on job listings is weekly and more timely than the BLS series. The last datapoint is for the week of December 31. It shows openings down 30% from the March 2022 peak and only 25% higher than the 2019 average."

............... Those who believe the U.S. can't go into recession when the jobs market is still strong, don't know their history. During the inflationary recessions of the 1970s, the jobs market always rolled over long AFTER recession had already begun:

......

The Great Demographic Reversal?

...........

9. Conclusion

In sum, the theoretical construct of pure inflation is of no use in understanding the price events of 2021 and 2022 in the United States. By extension, the conventional tools of the Phillips Curve, NAIRU, potential output, and money-supply growth are equally useless. By further extension, the “anti-inflation” policies of the Federal Reserve have acted on asset markets (which are not part of theoretical inflation) while taking credit for the end to a price process in produced goods that was transitory in any event. Yet the Federal Reserve is now stuck in a posture guaranteed to destabilize economic activity sooner or later, while the economy remains vulnerable to additional potential price shocks emanating from the same sources already seen, including real resources, supply chains, wars, pandemics, and the policies of the Federal Reserve itself. These can be dealt with, if at all, only by policies in each specific area ...

It takes a lot of motivated reasoning to believe otherwise.

Vid Fare:

Bubble Fare, Old and New:

Tulipomania!

On Holland’s legendary tulip bubble, which burst today in 1637

On Holland’s legendary tulip bubble, which burst today in 1637

Investors need to take a cold shower

Quotes of the Week:

Thorne: BLS does the work for us but so few actually look at the report and anchor off the headline number. If you remove the population control effect and compare (apples to apples) December to January the Jobs create was 84k.

Thorne2: The hidden lead in all this noise is that Powell and the Streets fixation with Volcker is misplaced. To be blunt, one can easily say that Volcker is a false prophet. With the coming policy mistake, the Fed will win ST battle wrt inflation but lose the LT war on deflation

"The more he talked, the more dovish he was,” Charles-Henry Monchau, chief investment officer at Banque Syz, said of Powell’s briefing. “It’s possible we’ll continue to see a series of volatility, but definitely the conditions seems to be more risk-on than last year,”

Charts:

1:

3:

🇺🇸 Not sure what's going on here 🤔 pic.twitter.com/OWCESvvDhe

— Mikael Sarwe (@MikaelSarwe) February 3, 2023

...

...10Y still inside the wedge. If it breaks down, it's short covering time for bond shorts. Bonds are one of the MOST shorted asset classes of ALL!

— Fibonacci Investing⚡️ (@FibonacciInves1) February 1, 2023

Long $TLT pic.twitter.com/blRL4OQ94B

Mean revision on the 10Y would put it at around 1.9%. That would still translate to about 140 on $TLT. That's in the soft landing scenario. That lines up with about 2024 expected CPI with no discount or premium applied. pic.twitter.com/M3j0RUVoeg

— Fibonacci Investing⚡️ (@FibonacciInves1) February 4, 2023

(not just) for the ESG crowd:

Deep in the DNA of an Antarctic octopus, scientists may have uncovered a major clue about the future fate of the continent’s ice sheet – raising fears global heating could soon set off runaway melting.

Climate scientists have been struggling to work out if the ice sheet collapsed completely during the most recent “interglacial” period about 125,000 years ago, when global temperatures were similar to today.

The ice sheet holds enough water to raise sea levels by 3 to 4 metres with fears that global heating could soon push it towards runaway melting that would lock-in rising sea levels over centuries. ......

Effluent limitations guidelines may be revised as a result

Astronomers Say They Have Spotted the Universe’s First Stars

Other Fare:

Theory has it that “Population III” stars brought light to the cosmos. The James Webb Space Telescope may have just glimpsed them.

Other Fare:

Education has become an investment. But what are its returns?

Higher education in the United States is a speculative endeavor. It offers a means of inching toward something that does not quite exist but that we very badly want to realize—enlightenment, higher wages, national security. For individuals, it provides the lure of upward mobility, an illusion of escape from the lowest rungs of the labor market. For the federal government, it has charted a kind of statecraft, outlining its core commitments to military strength and economic growth, all the while absolving the state of the responsibility for ensuring that all its subjects have dignified means to live. We are told the path to decent wages and social respect must route through college.

The metric of higher education is credit; it runs on the belief of future value amid present uncertainty. This has readily lent to the industry’s financialization, the elaborate ways of using money to make more money rather than to produce goods and services. Today financialized systems of higher education mean that colleges and universities operate as investors or borrowers or both. University revenues increasingly come from financial activities, such as profits from endowment investments, real estate acquisitions, or leveraging student tuition. Simultaneously, financial costs—such as debt, interest, and fees—command a growing portion of university expenditures. ......

How we became the tyrants of the animal kingdom

Pics of the Week:

Pics of the Week:

Visual effects artist is amazing! pic.twitter.com/XU9qRdgfjh

— The Figen (@TheFigen_) February 3, 2023

No comments:

Post a Comment