MP3 created a self-reinforcing demand explosion that is getting harder, not easier, for supply to keep up with.

Even as supply disruptions and higher inflation persist, markets are discounting that they will soon subside, leaving inflation at central bank targets and allowing for very easy monetary policy for a very long time. We disagree. While the headlines tend to focus on the micro elements of the supply shock (the LA port, coal in China, natural gas in Europe, semiconductors globally, truckers in the UK, etc.), this perspective largely misses the macro cause that is likely to persist and for which there is no idiosyncratic solution. This is not, by and large, a pandemic-related supply problem: as we’ll show, supply of almost everything is at all-time highs. Rather, this is mostly an MP3-driven upward demand shock. And while some drivers of higher inflation have been transitory, we see the underlying demand/supply imbalance getting worse, not better.

The mechanics of combined monetary and fiscal stimulus are inherently inflationary: MP3 creates demand without creating any supply. The MP3 response we saw in response to the pandemic more than made up for the incomes lost to widespread shutdowns without making up for the supply that those incomes had been producing. This is very different than post-financial-crisis MP2, where QE, by and large, was not paired with significant fiscal stimulus but instead offset a credit contraction and, as a result, was not inflationary.

We’re now seeing the inflationary mechanics of MP3 play out and observing just how potent a tool it is. And while the composition of the demand it fueled will evolve (e.g., shift from goods back toward services as COVID recedes), demand is likely to remain highly elevated. There are still large stockpiles of latent spending due to the transformative effects that MP3 has had on balance sheets and the ongoing incentive provided by extremely low real yields, and more fiscal stimulus is on the way. Choking off demand would require central banks globally to move toward restrictive policies quickly, which looks unlikely.

In this research, we paint a picture of the surge in demand and how supply is straining to meet it virtually everywhere you look. There are not enough raw materials, energy, productive capacity, inventories, housing, or workers. We start with this broad-brush picture because the demand-driven nature of the problem results in a game of whack-a-mole: alleviating a shortage in one area will likely just exacerbate the problem elsewhere in the supply chain.

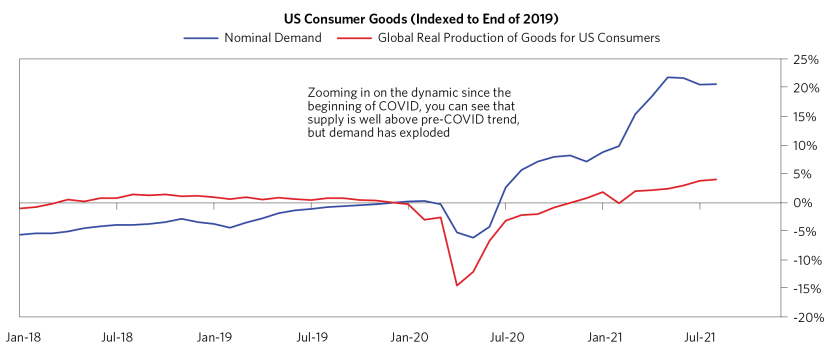

Goods Production Is Well Above Pre-COVID Trend, but Demand Has Exploded

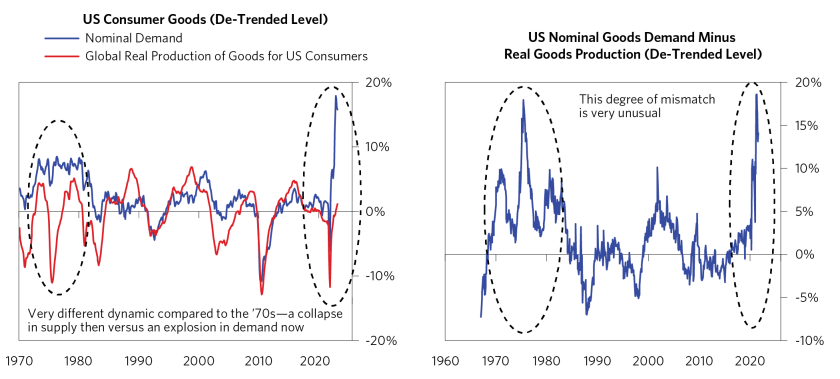

Supply has recovered remarkably quickly. As you can see in the top chart, real goods production is now higher than it was pre-COVID. The issue is that demand has exploded, creating an imbalance of a magnitude that we haven’t seen since the 1970s. The bottom charts show the current imbalance in historical perspective. What happened in the ’70s truly was a supply shock: supply collapsed, and demand stayed relatively steady. Today, demand is surging, and supply is also growing, but it just can’t keep up with demand.

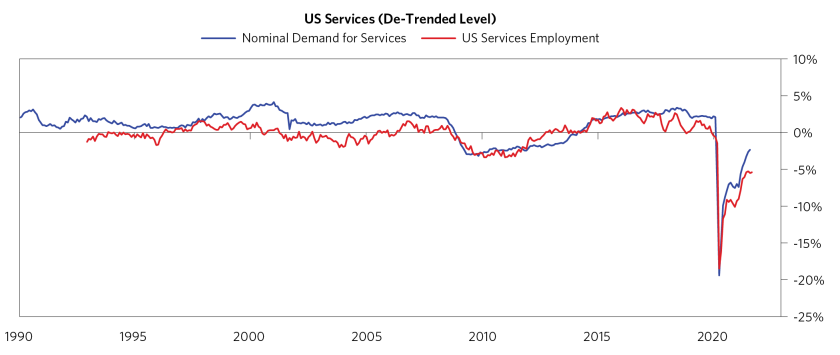

While some of the goods demand is unlikely to persist because of the unique circumstances of COVID prompting people to shift their spending from services to goods, the problem of shortages is also happening for services and is likely to build. The chart below shows that demand for services is rapidly returning to pre-COVID levels and services employment is lagging, as employers are having trouble finding workers.

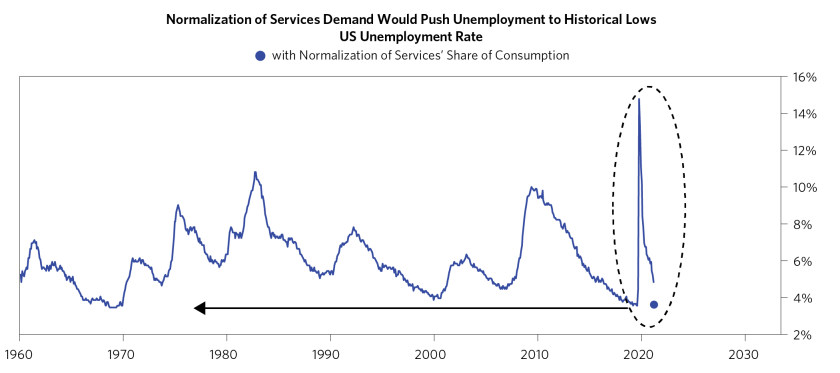

As services demand continues to normalize, that will put more pressure on a labor market that is already very tight (as we’ll get into more below). As a rough size of the magnitude of the problem, if you take the typical relationship of how much labor it takes to satisfy services demand, a return to pre-COVID levels of services demand would push unemployment to historical lows. Addressing this imbalance will mean placing upward pressure on wages to entice more workers to work longer as well as requiring investment to improve productivity.

Given the cause of massive demand, addressing these shortages is like a game of whack-a-mole. You can fix it in one place, but you can’t fix it everywhere in any simple way. It’s going to require a lot of investment and/or a lot of productivity enhancement to catch up. But right now, the gap is so large—and policy remains so loose that it’s encouraging demand further—that this gap is likely to be reasonably sustained.

In terms of household demand, we’ve described in detail how Monetary Policy 3 created a lasting transformation. Governments transferred a massive amount of cash to households, more than offsetting lost income from COVID. Household balance sheets are now in a materially better state than they were pre-pandemic, as MP3 created a significant amount of wealth, pushing up the value of assets like equities, housing, cryptocurrencies, and so on. These gains have been broad-based across the economy, not just in the top decile or quantile. Ongoing stimulative financial conditions have further lowered debt service costs, and incomes have also benefited as economies have reopened. In short, households are wealthy, flush with cash, and ready to spend—setting the stage for a lasting, self-reinforcing surge in demand.

Below, we go granularly across the supply side, reviewing each set of shortages and price increases we’re seeing in the economy today. While each case has its own idiosyncratic drivers, in all of them, the level of demand is outpacing the level of supply, which is higher than pre-COVID levels. As a result, prices are rising and will likely continue to do so unless there is a significant boost in productivity so supply can catch up with demand, or policy makers shift to a tighter stance in order to reduce demand.

There Are Not Enough Raw Materials

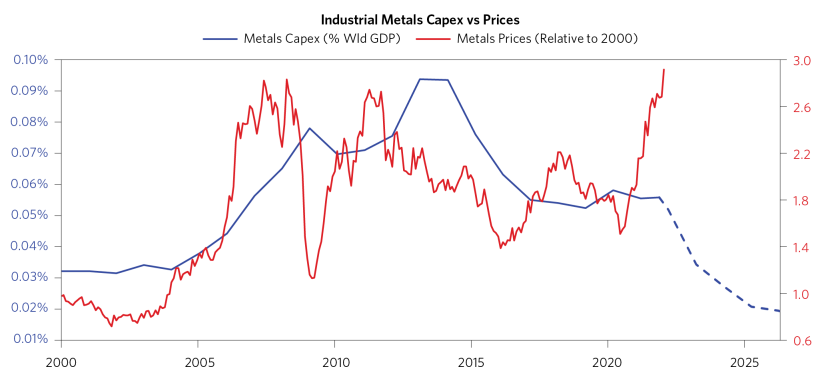

Metals prices have risen sharply since last year, as demand has far outstripped supply. Looking ahead, it will be hard to bring supply online because of the significant underinvestment in capex spending over the past decade, and capex spending itself will be a further strain on limited resources. In fact, capex remains muted even now that prices and demand for non-fuel commodities are back to or above pre-pandemic levels. Some commodities, most notably US shale, can ramp up quickly. But many can take up to 10 years to bring new capacity online, so shortages are likely to persist.

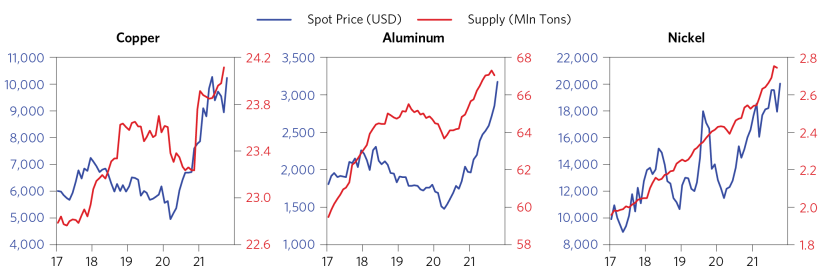

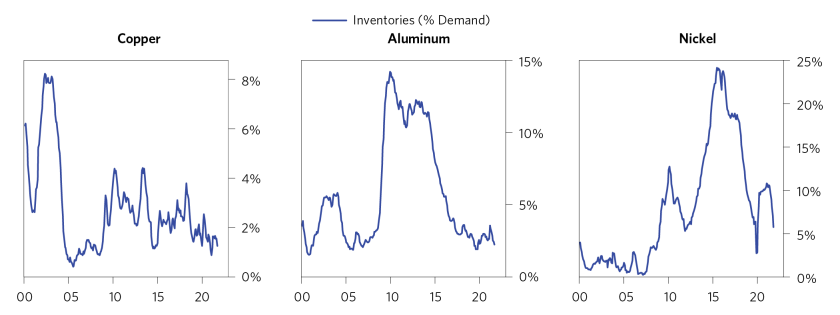

Looking at examples of individual markets triangulates the picture that the price increases are due to demand, not supply. For copper, aluminum, and nickel, supply is much higher than in recent years, but prices are still rising, and inventories are being driven down.

There Is Not Enough Energy

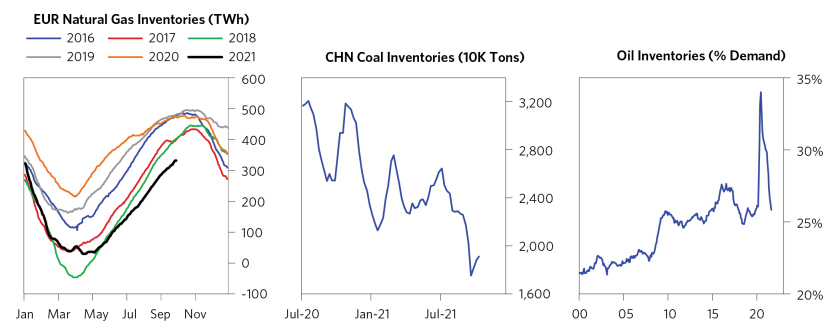

Similarly, there’s not enough energy to power economic activity given the current levels of demand. Prices of natural gas, coal, and oil are all spiking, all around the world. There are idiosyncratic constraints on supply, such as environmental regulations on coal in China or Russia restricting natural gas exports to Europe. But prices are rising across the board because demand is surging, and that demand is eating into inventories despite reasonable levels of production.

There Is Not Enough Productive Capacity

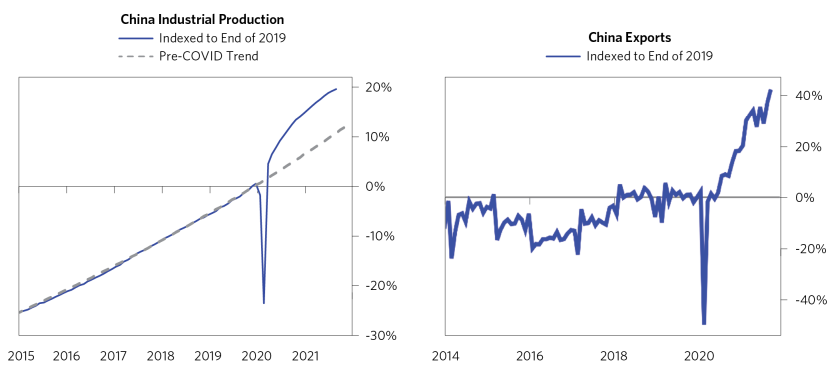

To keep up with the surge in demand, global production has risen above trend, as shown earlier. Most of the marginal productive capacity has come from China, which has ramped up its production significantly above pre-COVID trend, but there is a limit to how much it can stretch. Chinese production is 20% higher, and exports a full 40% higher, than at the start of 2020. (This is why there’s not enough coal in China—massive global demand has created a massive need for energy.)

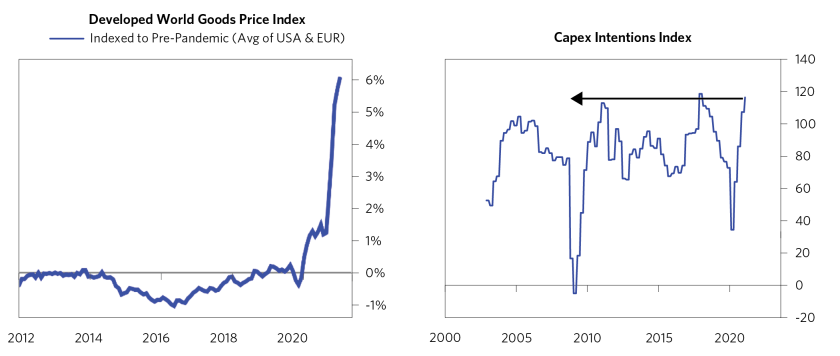

Yet despite this surge in supply, it’s still not enough to keep up with demand. As a result, developed world goods prices are exploding because demand has pushed the global supply chain to extremes. In response, capex intentions are at highs in order to try to deal with these pressures. And while capex will create a source of supply in the long term, it’s another source of demand that will contribute to the ongoing squeeze in the short term.

There Is Not Enough Inventory or Shipping Capacity

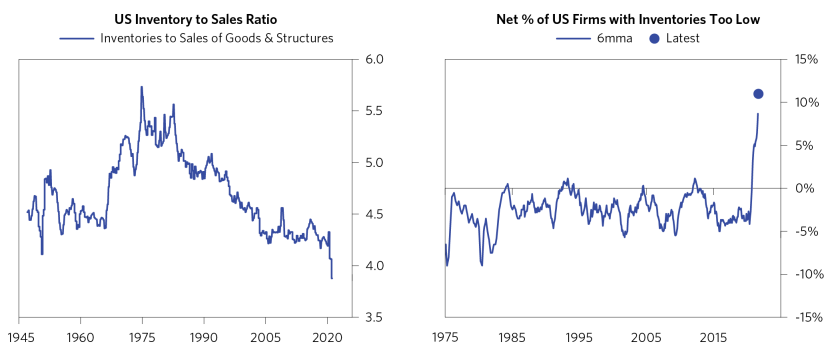

The same problems pop up as you move up the supply chain. There wasn’t enough production, and now very few firms have enough inventory, which will have to force a change in mindset. After decades of holding low levels of inventory to prop up margins and firms expecting to be able to get necessary supplies quickly when they need them, those assumptions are breaking down. Inventories across the economy have collapsed to historically unseen levels, with the net percentage of US firms who think the total inventories are too low now massively higher than anything we’ve seen since 1975. And while drawing down inventories was a way to provide enough supply to keep up with strong demand on a backward-looking basis, firms no longer have that option, and it will be even harder to satisfy forward-looking demand.

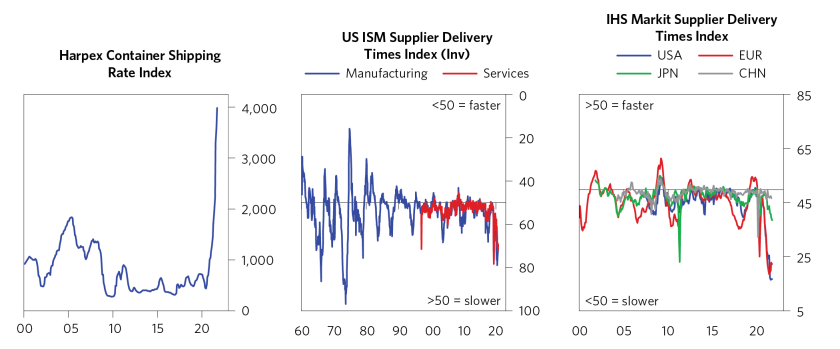

In addition to having low inventories, it’s now much harder for businesses to get supplies delivered when they need them. Across a range of different measures, shipping costs and shipping delivery times are much higher.

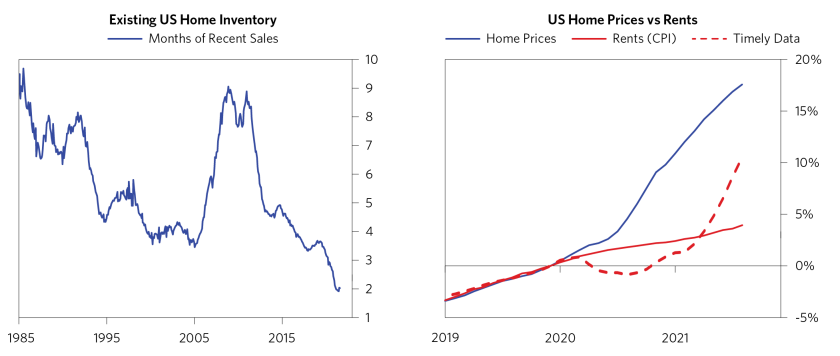

There Is Not Enough Housing

Housing is an example where pricing pressures aren’t fully reflected yet in recent inflation stats because of quirks in CPI reporting, and it will be a critical inflationary pressure moving forward. Ultra-low real interest rates and improving wages are supporting a sustained housing boom, and supply just hasn’t been able to keep up: in the US, housing inventories have fallen to levels far below anything seen in recent history. As a result, home prices are surging. Rents are also surging, though rents reported in CPI numbers are lagging this rise—a future support to CPI levels going forward.

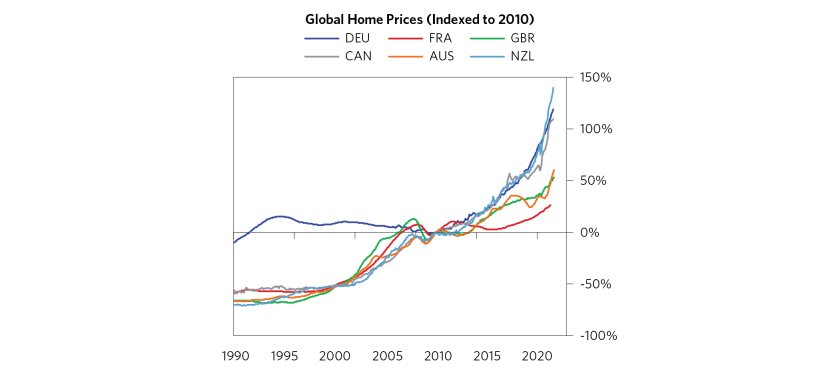

This isn’t just a US phenomenon either. Normally, there are more divergences among global housing than there are today. Prices are elevated everywhere because of the incentives of the MP3 world—extremely low interest rates and a tight job market (which is particularly tight in the US but is getting tighter in the rest of the world as well).

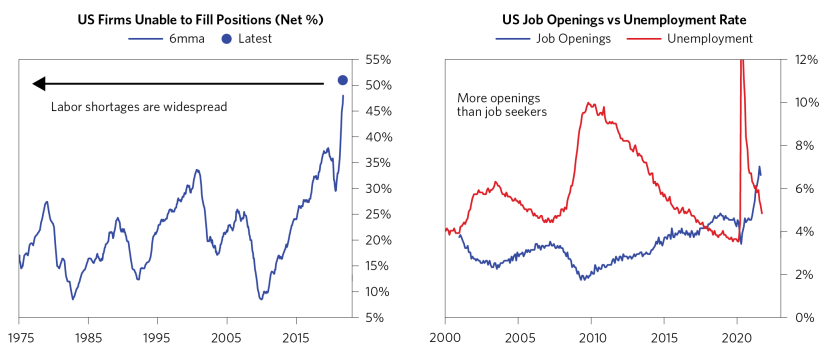

There Is Not Enough Labor

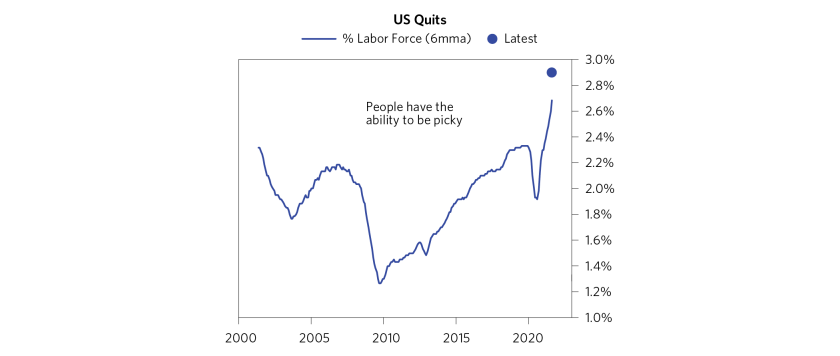

And finally, there’s labor. We have not seen a labor market this tight in our lives. This is nothing like the boom in the 1990s or 2006-2007 or even pre-COVID. Half of all firms in the US are unable to fill their positions—far higher than anything we’ve seen since 1975. There are more job openings than there are unemployed people by a decent degree. And workers are demonstrating the new leverage they have—the quits rate is the highest it’s been in the history of the data.

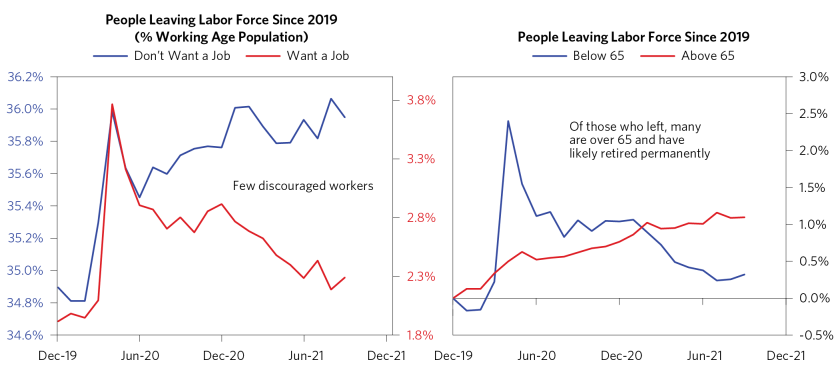

Further, those who left the labor force during COVID don’t seem particularly likely to come back, as most say they don’t want a job, and many are over 65 and are likely permanently retired—these folks would need to be enticed to come back into the job market.

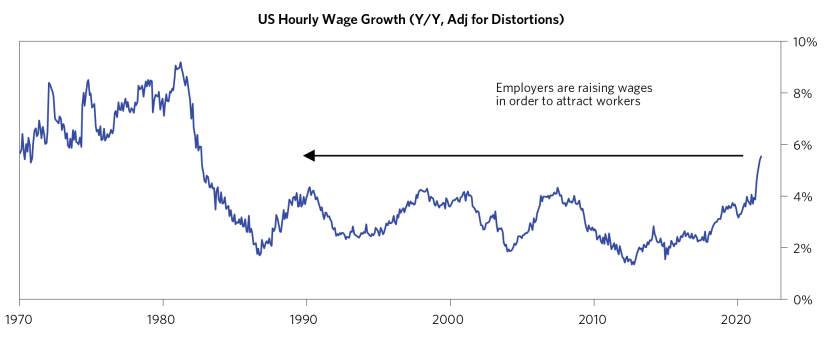

All of these pressures combined are leading wages to rise at the fastest rate since the early 1980s, as demand is far exceeding the supply of labor. In our view, these wage increases are only the beginning of the next major wave of inflationary pressures. For starters, as consumers’ spending behaviors revert toward pre-COVID patterns, thereby increasing spending on labor-intensive services, the ongoing shortage of labor will worsen. And as expectations of higher inflation start to get baked into future wage increases, inflation will become increasingly self-reinforcing, with no easy way out.

With demand outstripping supply everywhere you look, policy makers are unlikely to be able fix shortages across the board. They can open ports for longer, as in the US, or ease environmental regulations, as in China, but in order for supply and demand to clear at levels that don’t lead to sustained price increases, there would need to be a massive investment in productivity for supply to catch up. The gap between demand and supply is now large enough that high inflation is likely to be reasonably sustained, particularly because extremely easy policy is encouraging further demand rather than constricting it.

No comments:

Post a Comment