*** denotes well-worth reading in full at source (even if excerpted extensively here)

Economic and Market Fare:

Hunt: Quarterly Review and Outlook (pdf)

.... Although Friedman’s monetary theory of inflation has justifiably drawn criticism, major components of his theory of interest rate cycles remain intact and the so-called flawed aspect can be overcome by converting money velocity (V) to an endogenous variable rather than assuming that V is stable. Once restated, the model applies very directly to the current interest rate outlook and suggests that even though the Fed is planning further increases in the federal funds rate in 2023, the direction of long-term U.S. Treasury rates is downward. In this letter, we will modify Friedman’s theory to incorporate an endogenous V and then apply the new model to the situation at hand as well as to the tumultuous events of the past three years. The determinants of velocity to be identified serve to reinforce the view that the U.S. Treasury bond market’s prospects are favorable even though conditions are very likely to remain volatile. .......

Final Thoughts … The better growth in real GDP experienced in the third quarter and early part of the fourth quarter will reverse. Poor consumer spending over the critical Christmas shopping period, slumping exports, sharp deterioration in residential construction, and contracting diffusion indices in both the manufacturing and service sectors will result in business conditions in the first quarter that should be dramatically weaker than the fourth quarter. The risks of recession will become much clearer as 2023 progresses. Headline inflation will recede further from the 1.9% pace in the CPI of the latest six months. These developments are aligned with interest rate cycle theory as well as the case for lower U.S. Treasury bond yields.

US Layoffs Far Higher Than Suggested By Initial Jobless Claims, JOLTS

.... But while one can certainly appreciate Biden's desire to paint the glass of US jobs as always half full, reality is starting to make a mockery of the president's gaslighting ambitions, as one by one core pillars of the administration's "strong jobs" fabulation collapse. First it was the Philadelphia Fed shockingly stating that contrary to the BLS "goalseeking" of 1.1 million jobs in Q2 2022, the US actually only added a paltry 10,000 jobs (just as the Fed unleashed an unprecedented spree of 75bps rate hikes).

And now, it is Goldman's turn to make a mockery of the "curiously" low initial jobless claims, by comparing them to directly reported WARN notices which no low-level bureaucrat and Biden lackey can "seasonally adjust" because there they are: cold, hard, fact, immutable and truly representative of the underlying economic truth. So what is said truth? ..............

.... And while the WARN data clearly indicate that both claims and JOLTS data is misrepresenting the underlying economic reality in an overly cheerful manner, the silver lining is that the bank's findings are consistent with recent survey results from the Conference Board, which have signaled that company executives would be more reluctant to lay off workers than in typical downturns. Of course, that is all contingent on the coming recession being shallow, a concept which as we discussed before, is at best idiotic.

Thomas: The 10 Charts to Watch in 2023

The key macro/market charts for navigating risk vs opportunity this year...

1. Global Recession 2023: One of the most interesting pieces of work I undertook in 2022 was to perform a sort of meta-analysis on all the leading indicators I’ve developed over the years. The key takeaway from that is whether you group leading indicators by type/factor, geography, or forecast window — they are all unanimous in pointing to a sharp downturn heading into early-2023.

In many ways it’s a coming full circle of the massive stimulus that was unleashed in 2020. Or as I call it: “a strange but familiar cycle”.

Overall: I would repeat my quip of this being a “strange but familiar cycle”, particularly in that a lot of the usual macro/asset allocation sign posts that we usually follow continue to work and are pointing fairly clearly to the next steps. Hence from an asset allocation standpoint I would be overweight defense (cash and government bonds) vs underweight growth assets (equities, commodities, credit) given how things sit at the moment.

Inside the High-Yield Spread

High yield is not pricing a recession

The Observatory: Real GDP Contraction

Welcome to The Observatory. The Observatory is how we at Prometheus monitor the evolution of the economy and financial markets in real-time. The insights provided here are slivers of our research process that are integrated algorithmically into our systems to create rules-based portfolios.

Real GDP, profits, and the labor market are at a critical juncture in the economic cycle. Today, we received significant data updating our tracking of economic conditions. First, we received retail sales data, which decreased -1.15% in December, disappointing consensus expectations of -0.9%. This print contributed to a sequential deceleration in the quarterly trend relative to the yearly trend ........

.......... Overall, data continues to evolve in line with a slowdown, which will drive profits lower, which and push labor markets lower. Amidst such an environment, market pricing of growth is likely to deteriorate significantly.

The Beginning Of The End Of The Credit Cycle

The credit cycle is turning, which points to wider credit spreads, increasing loan-losses at banks, and rising equity volatility.

Credit has exploded higher since the pandemic. But all good things must come to an end, with credit busts typically following close on the heels of credit booms. Cracks are now emerging in lending markets as the sharpest monetary policy tightening in decades begins to bite.

The recent expansion in credit was across the board, from leveraged and private loans to corporate debt and bank loans. ....

.......... Loan and corporate-debt issuance has slowed this year compared to last, but the penny has not yet dropped that the credit cycle is on the cusp of turning, and could deteriorate significantly in the coming quarters - turbocharged by an impending recession. As always in markets, pay attention to what is going to happen, not what is happening, and prepare accordingly.

The US Consumer Has Cracked: Discover Plunges After "Shocking" Charge-Off Forecast

Car-mageddon?? Auto Insider Predicts Car Prices To Fall This Year

High-frequency truckload data suggests the freight market is stabilizing

............................ On the other side of the pond, the situation is different. The Federal Reserve has raised interest rates substantially throughout last year and, different than the ECB, has already begun to shrink its balance sheet. Monetary policy measures have already led to deflation, which means a shrinking money supply. Thus, in the original definition, the US entered a period of deflation in March 2022.

Roberts: Wages, prices and profit – turning down

The inflation rate for consumer prices in the US has clearly peaked and is falling steadily. The latest figure for year-on-year inflation in December was 6.4%, down from a peak of 9.0% last summer. Core inflation (which excludes prices for food and energy) has also peaked but not by nearly as much. That’s because it is food and energy price inflation that has slowed the most. Energy price inflation has halved as oil and gas prices drop back and there has been a peak in food prices. But housing costs continue to accelerate and other services prices fell only a little; so core inflation remains ‘sticky’. ......

[I]nflation in the midst of stagnation is not an anomaly.As much of the world grapples with post-Covid price gouging, it seems like a good time to revisit our understanding of inflation. In this post, I’m going to test Jonathan Nitzan and Shimshon Bichler’s ‘stagflation thesis’.

If anything, it is the general rule.

— Nitzan and Bichler, 2009

The idea is that ‘stagflation’ — economic stagnation combined with high inflation — is not some exogenous ‘market shock’. According to Nitzan and Bichler, stagflation is a business strategy — one of two main routes to profit.

The first route to profit is for businesses to hold prices steady while they try to sell more stuff. The second route is to jack up prices. Since this latter option requires restricting the flow of resources (stuff that flows freely cannot be dear), Nitzan and Bichler reason that when inflation rears its head, it ought to come with economic stagnation. In other words, stagflation is the norm.

If this stagflation thesis is correct, then inflation ought to correlate negatively with economic growth. Looking at the United States, Nitzan and Bichler find evidence that it does. Here, I broaden their stagflation research by looking at all countries in the World Bank’s global development database.

I find that both within and across countries, economic growth (measured in terms of energy use) tends to decline as inflation increases. So Nitzan and Bichler appear to be onto something. Over the last half century, stagflation is the general rule. ........

Quotes of the Week:

as a buyer of some ZROZ on morning of Jan 19, same morning he wrote this, obviously I disagree here:

Clark: Putting it all together, what do I think? I think that buyers of TLT US and 30 Year treasuries are hungry for punishment. And I am pretty sure the market is going to dish it up for them.

Charts:

1:

Bubble Fare:

The Current Housing Price Bubble "Makes 2008 Look Quaint"

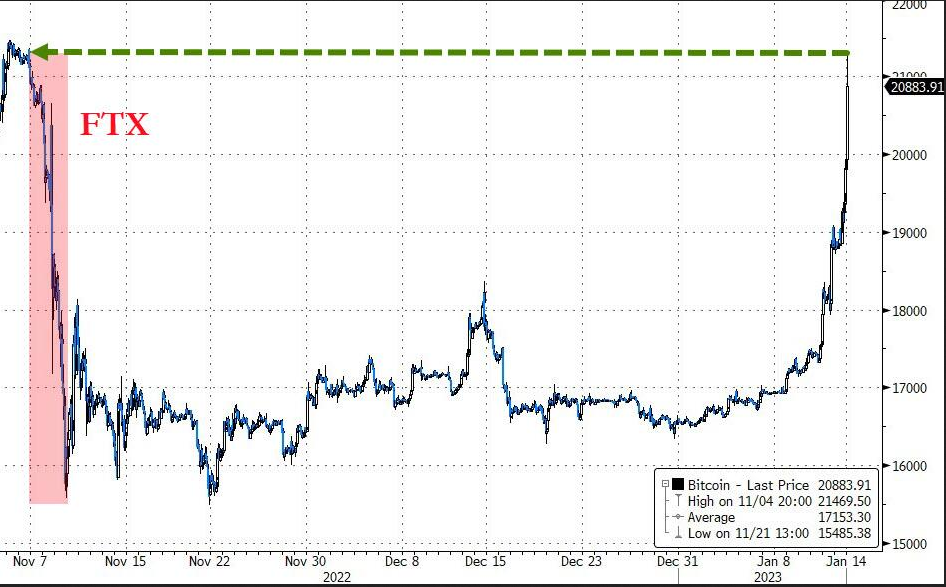

Bitcoin Rally To $21K Prompts Analysts To Ask Where BTC Price Will Go Next

BIS: Addressing the risks in crypto: laying out the options (PDF)

(not just) for the ESG crowd:

The Carbon Con

The world’s biggest companies, from Netflix to Ben & Jerry’s, are pouring billions into an offsetting industry whose climate claims appear increasingly at odds with reality

EWG study: Eating one freshwater fish equals a month of drinking ‘forever chemicals’ water

PFAS found at high levels in freshwater fish, with most concern for vulnerable communities

‘Extinction crisis’ of sharks and rays to have devastating effect on other species, study finds

Ion-Air Batteries 10 Times Cheaper Than Li-Ion Will Start Mass Production in 2024

EVs are getting too heavy and too powerful, safety chief says

Not Sure Where to Place This, but well worth reading, Fare:

Why China’s Shrinking Population Is a Big Deal – Counting the Social, Economic and Political Costs of an Aging, Smaller Society

read, in particular, Yves' prefatory remarks, including her excerpt of IMDoc's comments

Older Stuff:

Inside the Tow Truck Mafia: How Organized Crime Took Over Canada’s Towing Industry

Back alley deals, fake crashes, arson, and even murder—nothing is off limits in the ruthless world of Canada’s towing companies.

When most people think of organized crime, they probably picture Tony Soprano’s “waste management” gig, the various drug cartels, or the body counts racked up by the Mafia in cities like New York and Chicago in decades past. But for the people living in Canada's most populous province, organized crime takes a very different but very real form: Towing. Yes, towing. Criminal enterprises have run rampant across Ontario's towing industry since at least the early 2000s, and the situation has resulted in unlawful tows, firebombs, and even murders across the Greater Toronto Area.

Other Fare:

What's behind Canada's drastic new alcohol guidance

In Canada, it should be Dry January all year round, according to new national recommendations that say zero alcohol is the only risk-free approach.

If you must drink at all, two drinks maximum each week is deemed low-risk by the government-backed guidance.

The advice is a steep drop from the previous recommendation, published in 2011.

Those guidelines allowed a maximum of 10 drinks a week for women and 15 drinks for men.

Vid Fare:

Animal Justice With Martha Nussbaum

Pics of the Week:

Pooch portraits: Dog Photography awards – in pictures

The winners of the 2022 Dog Photography awards, chosen from more than 1,400 entries from 50 different countries

No comments:

Post a Comment