*** denotes well-worth reading in full at source (even if excerpted extensively here)

Economic and Market Fare:

The key macro/market charts for navigating risk vs opportunity this year...

1. Global Recession 2023: All leading indicators continue to point to recession, and there has been nothing to negate or confound that signal. If anything, the banking crises only raise the prospect and proximity of a steep global economic recession.

“One of the most interesting pieces of work I undertook in 2022 was to perform a sort of meta-analysis on all the leading indicators I’ve developed over the years. The key takeaway from that is whether you group leading indicators by type/factor, geography, or forecast window — they are all unanimous in pointing to a sharp downturn heading into early-2023. In many ways it’s a coming full circle of the massive stimulus that was unleashed in 2020. Or as I call it: “a strange but familiar cycle”.” ......'

The US economy may be on the brink of a recession if an early sign of distress in the credit markets is anything to go by.

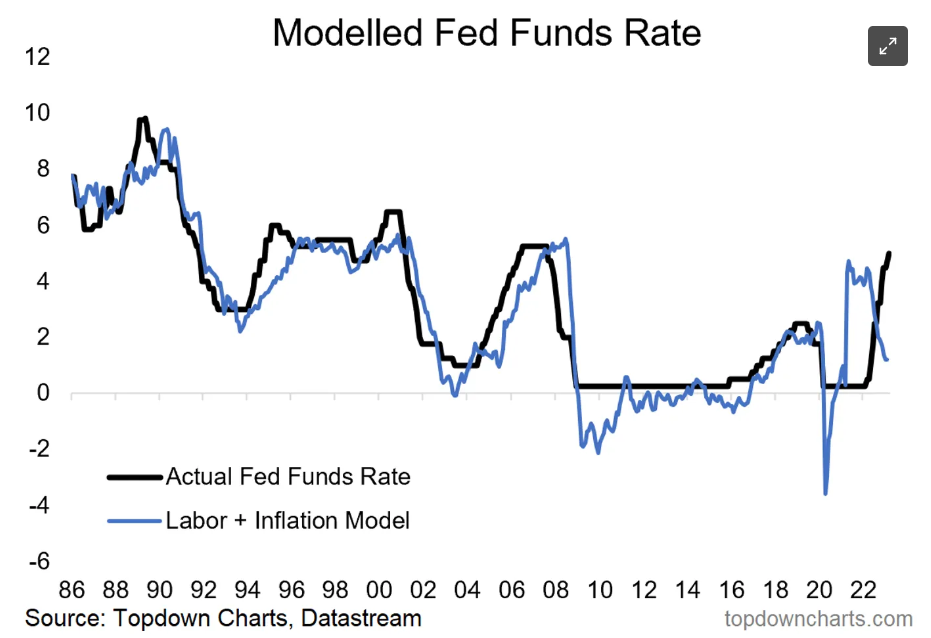

The chart below shows the implied path of the Fed funds rate based on a broad composite of inflation expectations and labor market indicators (over 20 individual data series — which serve to amplify the true signal vs noise).

We can clearly see how it was justified for the Fed to cut rates into the pandemic (perhaps even more than it did)… but that they should have removed the emergency measures shortly after reopening. Instead, they made an active decision to take the risk of overcooking growth/inflation/speculation vs the risk of tightening too early and potentially scuppering the nascent recovery.

A direct consequence of all this and everything else that’s gone on over the past year is the various leading indicators for the US economy have plunged to record lows (very high risk of recession now), so the Fed will probably need to pivot later this year as it continues to fight yesterday’s battle. But that will not be good news — contrary to popular narratives — because by the time it becomes obvious (and because of 1970’s inflation fears affecting decision making biases: it will need to be obvious) recession will already be underway.

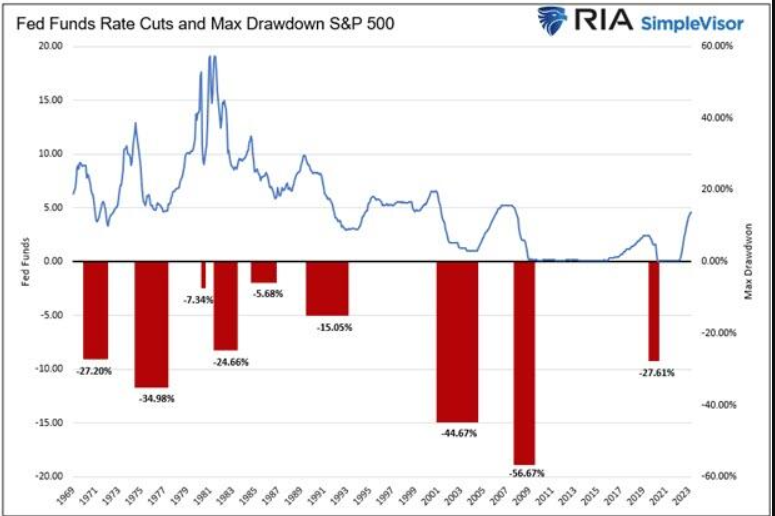

But there are several reasons why there could be another abrupt alteration in the state-of-play, with the first cut coming as early as June, and potentially significant cuts priced in before the end of the year:

- Signs of deterioration in the job market that gain momentum very quickly;

- A recession that now looks unavoidable and could begin as early as June;

- Inflation that is long past its cycle peak; and

- A rapid fall in velocity leading to a stock-market selloff

One of the surprising aspects of this cycle has been the resilience in the labor market. But that looks about to change. Unemployment claims are one of the most leading measures of the job market. The headline number has remained low, but the real information content comes from looking under the surface. ...

An old saying cautions one to be careful of what one wishes for. Stock investors wishing for the Federal Reserve to pivot may want to rethink their logic and review the charts. ... Like Pavlov’s dogs, investors buy when they hear the pivot bell ringing. Their conditioning may prove harmful if the past proves prescient. .........

................ The CRE loan risk is yet to hit. But it will hit the regional banks, already reeling, the hardest. And it’s a vicious spiral. CRE defaults hurt regional banks as falling office occupancy and rising interest rates depress property valuations, creating losses. In turn, regional banks hurt the real estate developers as they impose stricter lending standards post-SVB. This deprives commercial property borrowers of reasonably priced credit, crimping their profit margins and pushing up defaults.

When Silicon Valley Bank went down, many progressives, and much of the media, immediately pointed to malfeasance, special pleading and regulatory failures—a conditioned response with a strong pedigree. But if those were the real causes, then SVB (and Signature, and First Republic) would have been isolated cases. It’s clear now that they were not. A systemic crisis is unfolding—with a systemic cause. .......

................. So why did the Federal Reserve invert the yield curve? To fight inflation? To kill jobs and stall wages? If so, the stupidity—or the economistic groupthink—is shocking. .............

....... The money will flow into the United States. Into the money market funds and the biggest banks. Enhanced swap lines—to keep dollars available to foreign central banks—were trotted out on Sunday. They signal that the dollar is still boss, and also that the entire global banking system, indeed most of the world economy—outside of China and Russia—is fragile. Hold on tight.

*** Rubinstein: The Secret Diary of a Bank Analyst

Plus: Silicon Valley Bank, Money-Go-Round, Liquidity Coverage Ratios

.... The first thing to understand about banks is that they operate a unique financial structure. Other companies borrow from one group of stakeholders and provide services to another. For banks, these stakeholders are one and the same: their creditors are their customers. Most customers don’t realise this and as long as their loan to the bank (traditionally called a deposit) falls within the scope of their national deposit insurance scheme, they don’t have to.

........ For an analyst, this structure complicates things. No use looking at the ‘enterprise value’ of the business – the traditional barometer for measuring a business’ worth – because the debt is the business. No use looking at cash flow statements which disentangle cash generated in operating activities from cash generated in investing and financing activities because the operating activities are the financing activities.1

Because it’s where the customers sit, if you want to understand a bank, you have to look at its balance sheet. As a bank analyst, I would often peer over in envy as colleagues covering other sectors would go on factory tours or visit flagship retail outlets. I’d stay at home and study bank balance sheets.

To some extent the balance sheet is the business. The rest is there simply to feed it – the store a device to attract new funding. Bank executives may not want to admit it because it seems overly reductive, but those that forget do so at their peril. ........

.... Banks have a licence to create money which confers on them a special status somewhere between private enterprise and public entity. Economists argue that commercial banks create money by making new loans. When a bank makes a loan, it credits the borrower’s bank account with a deposit the size of the loan. At that moment, new money is created.

Bank analysts don’t quite see the world like this. In their view, banks need deposits in order to make loans. ‘Deposits before loans’ is a more useful model for an individual bank. ........

...... Wherever you sit in a bank’s capital stack, make no mistake: a higher authority sits above you.

...... Most companies thrive on growth. “If you’re not growing, you’re dying,” they say. For investors, growth is a key input in the valuation process.

But if your job is to create money, growth is not all that hard. And if the cost of generating growth is deferred, because the blowback from mispricing credit isn’t apparent until further down the line, it makes growth even easier to manufacture. .........

....... The absolute foundation of banking is confidence. Depositors entrust their money to banks in the confidence that they will get it back according to the terms of their deposit.

As Matt Levine of Bloomberg’s Money Stuff writes (emphasis mine):

“The bank doesn’t just put your dollars in a box and wait for you to take them out; the bank uses its depositors’ money to make loans or buy bonds, and just keeps a little bit around for people who need cash. If everyone asked for their money back tomorrow, the bank wouldn’t have it. But everyone is confident that, if they ask for their money back tomorrow, the bank will have it. So they mostly don’t ask for it, so when they do, the bank does have it. The widespread belief that banks have the money is what makes it true.” ........

..... The dirty secret among bank analysts is that it’s quite hard for an outsider to discern what’s going on inside a bank. Former bank analyst Terry Smith knows it. “I think it is precisely because I understand banks that I never invest in their shares,” he wrote in the Financial Times last week. It’s only after the fact it becomes apparent what questions to ask. ......

***** Mitchell: When mainstream economists arrive at ideas 50 or so years late and pretend to be contributing to knowledge

.......................... The CEPR authors note that there is a recent literature that links monetary policy decisions taken by central banks to financial system stability and that low interest rate eras increase “financial fragility” over time.

There is also a long dated literature in Post Keynesian economics that ‘discovered’ the same thing (years ago).

Minsky any one?

But the astounding part of the CEPR article is their next claim:

Why, though, do money and credit expand in the first place? By analyzing this question, we contribute to the strand of the literature that focuses on potential causes of credit booms. To the best of our knowledge, this strand is relatively thin.

The reality is that the literature is, in fact, very rich on this topic.

Knut Wicksell

Axel Leijonhufvud

Basil Moore

Marc Lavoie

Augusto Graziani

Wynn Godley

and others, have all provided the original contributions in this field over many decades.

It is just that mainstream economists have ignored their work for all these years because by acknowledging it one has to jettison all the main precepts in mainstream monetary theory, which then leads to the conclusion that the dominant paradigm has nothing interesting or valid to say about policy design.

But now, in 2023, these German economists based at the University of Würzburg are claiming a contribution.

The problem is the horse already bolted – years ago.

Their contribution is really no contribution but merely a useful summary of the state of knowledge in Post Keynesian economic thinking. .........

Bubble Fare:

Beware: Artificial Intelligence Bubble

Quotes of the Week:

Wilson: When Markets Question the "Higher Powers," They Can Re-price Quickly: With bond markets questioning the Fed's dot plot, bond volatility has increased markedly. We think stocks are next as investors realize earnings guidance looks unrealistic. This is when the ERP typically reprices, and stocks may finally get ahead of the downside we see in earnings estimates.

................. “Our 21 Lehman systemic risk indicators are pointing at the highest probability of a crash or a sharp drawdown in the next 60 days—the highest probability since COVID,”.

McDonald believes investors are ignoring the risk of a “rolling credit crisis and focusing too much on the rise of new technologies like artificial intelligence"

Quotes of the Week:

Wilson: When Markets Question the "Higher Powers," They Can Re-price Quickly: With bond markets questioning the Fed's dot plot, bond volatility has increased markedly. We think stocks are next as investors realize earnings guidance looks unrealistic. This is when the ERP typically reprices, and stocks may finally get ahead of the downside we see in earnings estimates.

Rubinstein: The first thing to understand about banks is that they operate a unique financial structure. Other companies borrow from one group of stakeholders and provide services to another. For banks, these stakeholders are one and the same: their creditors are their customers. Most customers don’t realise this and as long as their loan to the bank (traditionally called a deposit) falls within the scope of their national deposit insurance scheme, they don’t have to.

Tweet Thread of the Week:

***** Concodanomics: The Great Financial Tightening has thrown the global monetary system into disarray, prompting large interventions by financial leaders. Markets perceived their response as a pivot, but it was just a stopgap. The real hard landing now awaits us... 1/

Ever since the great financial crisis in 2008, the system has been sculpted not by sound pre-planning of monetary policy, but by a series of experiments created during a myriad of crises. The response to the latest banking panic was just a taster of the Fed's financial alchemy...

...................

Markets quickly perceived this as the Fed initiating another round of quantitative easing (QE), the Fed's mechanism for injecting the most liquidity. In reality, however, it's far from it. With QE, the Fed buys bonds and issues reserves to pay for them. This was different...

Quantitative Tightening (QT) is still underway. The Fed hasn't bought bonds outright and is (at least) trying to lower the size of the balance sheet. The sudden pop in assets reflects attempts to paper over cracks while the Fed KEEPS tightening. This is Quantitative Teasing™...

...........

Just because the Fed's actions weren't QE, however, that didn't prevent a bullish message from being sent to risk assets. After all, it's not whether you understand QE's mechanics, it's what the crowd believes to be true. And the crowd deemed another driver more influential...

.........

The recent banking panic and the Fed's response to it reveal a pivot is now fully off the table. Monetary authorities will do everything in their power to maintain order during further tightening, without reversing course. And the most likely outcome is a hard landing.

Charts:

1:

(not just) for the ESG crowd:

Toxic Spills Have Impacted Two Waterways Near Pennsylvania & Minnesota, Leaving Residents To Ask: Is Our Drinking Water Safe?

Sci Fare:

Long COVID functional manifestations differ from post-vaccine effects

Patients with functional neurologic disorder (FND) after SARS-CoV-2 infection had different symptoms than people with FND after COVID vaccines, retrospective data showed. ....

AI:

Connor Leahy reverse-engineered GPT-2 in his bedroom — and what he found scared him. Now, his startup Conjecture is trying to make AI safe

There’s now an open letter arguing that the world should impose a six-month moratorium on the further scaling of AI models such as GPT, by government fiat if necessary, to give AI safety and interpretability research a bit more time to catch up. The letter is signed by many of my friends and colleagues, many who probably agree with each other about little else, over a thousand people including Elon Musk, Steve Wozniak, Andrew Yang, Jaan Tallinn, Stuart Russell, Max Tegmark, Yuval Noah Harari, Ernie Davis, Gary Marcus, and Yoshua Bengio.

Meanwhile, Eliezer Yudkowsky published a piece in TIME arguing that the open letter doesn’t go nearly far enough, and that AI scaling needs to be shut down entirely until the AI alignment problem is solved—with the shutdown enforced by military strikes on GPU farms if needed ........

Hanson: Robots-Took-Most-Jobs Insurance

I’ve long described the following as the most obviously helpful policy response to the possibility of advanced AI. But even though I’ve long known many folks who say they are very worried about AI, I have yet to motivate any of them to actually pursue this response. Let me now try again.

While far from obvious, it is plausible that someday machines may displace most all humans from their jobs. It is also not crazy to think that this might happen relatively suddenly, and without much warning. Which seems a pretty big problem, given that most people don’t own much more besides their ability to earn wages. Without some sort of charity or insurance, they might starve. Thus each of us seems well-advised to try to set up some insurance re this risk, instead of just hoping to rely on charity.

One needs to set up insurance well before problems are realized or revealed. Yet it can be hard to motivate people to insure against risks that seem too unlikely or remote in time. Which might make the current moment an ideal time to consider this. Many are now worrying loudly about AI, saying that AI might soon take all the jobs, or worse. And yet I’m pretty sure that most investors see this risk as actually still pretty remote and unlikely. Maybe making now a great time to set this up. ......

Other Fare:

Mary-Jane Rubenstein is a scholar of religion, but her latest book is about Jeff Bezos, Elon Musk, and the “corporate space race.” For Rubenstein, the promises that these men offer of a human future in vast colonies on Mars or the moon have much in common with religious myths of a “promised land.” And like these other myths, the ideology underlying Silicon Valley’s space colonization missions can be used to defend unjust acts in the here and now to serve the glorious long-term destiny of the species. Rubenstein’s new book, Astrotopia: The Dangerous Religion of the Corporate Space Race, looks at the ways in which stories about great destinies have been used to rationalize conquest and exploitation. Rubenstein worries that just as “Manifest Destiny” was used as an excuse for genocide in the United States, plans to “expand into space” will be used to justify trashing Earth and ignoring the most pressing issues of inequality in our near-term future.

Tweets of the Week:

Ten reasons why we should turn off ChatGPT: a thread

— Marco Piani (@Marco_Piani) March 26, 2023

No comments:

Post a Comment